BU247 Chapter 3: Chapter 3- Accumulating and Assigning Costs to Products

Document Summary

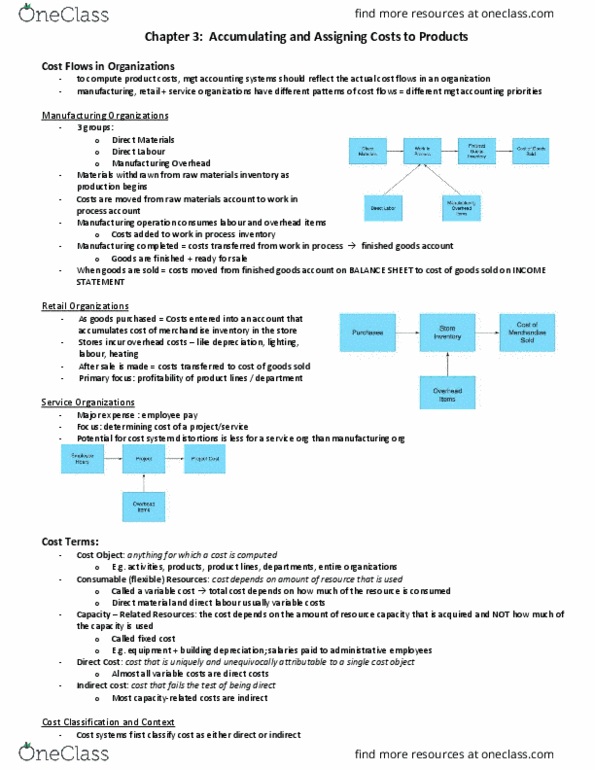

Bu247 chapter 3: accumulating and assigning costs to products. Cost management systems measure the costs of products, services, and customers. Job order costing and process costing used to cost products and services. Cost management systems differ in the way they assign indirect costs to cost objects. Materials withdrawn from raw materials inventory as production begins cost entered into production moved from raw materials account to work-in-process inventory account. When manufacturing is completed, work is transferred to finished goods inventory and costs are moved from work-in-process inventory account to finished goods inventory account. When goods are sold, their costs are moved from finished goods inventory to cogs. Idea behind manufacturing costing systems: to determine that products accumulate as they consume organization resources during manufacturing. As goods are purchased, their cost is entered into an account that accumulates the cost of merchandise inventory in the store stores incur overhead costs (e. g. labour, depreciation on store, lighting, heating)