BU247 Chapter Notes - Chapter 7: Sensitivity Analysis, Financial Institution, Cash Flow Statement

Document Summary

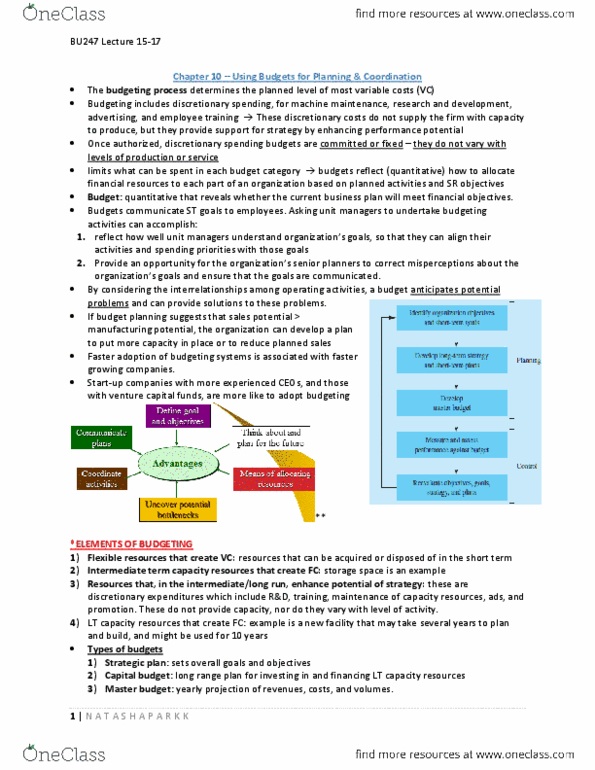

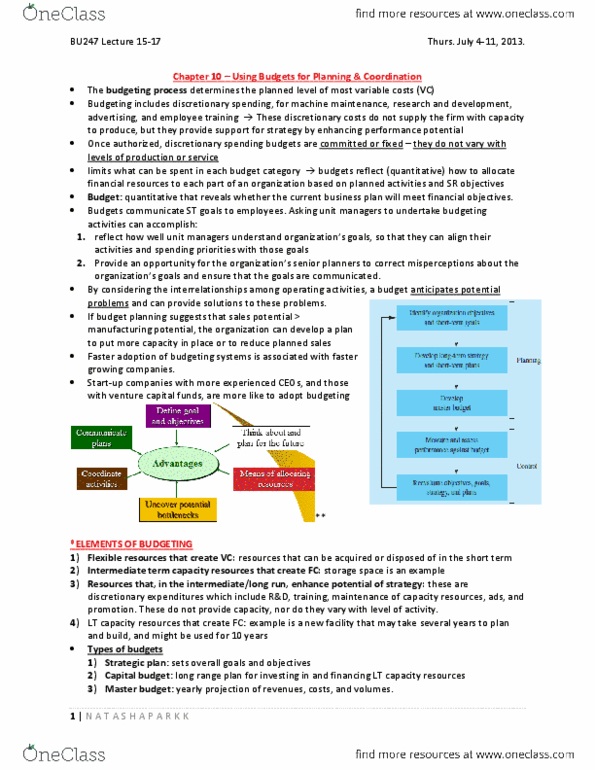

Bu247 chapter 7: using budgets for planning and coordination. Determining the levels of capacity-related and flexible resources. Variable costs: costs that varied with activity level in the firm. Fixed/capacity-related costs: costs that didn"t change with changes in activity level. For decisions affecting short term, firm"s fixed costs are considered given and fixed. Budgeting process: determines the planned level of most variable costs. Budgeting includes discretionary spending, such as for machine maintenance, r&d, advertising, and employee training don"t supply firm with capacity to produce, but provide support for organization"s strategy by enhancing its performance potential. Once authorized, discretionary spending budgets are committed or fixed, so they don"t vary with levels of production or service. Budgets are central part of design and operation of management accounting systems. Budgets in organizations reflect in quantitative terms how to allocate financial resources to each part of an organization based on planned activities and short-run objectives.