BU352 Chapter Notes - Chapter 11: Ebay, Demand Curve, Marketing

Document Summary

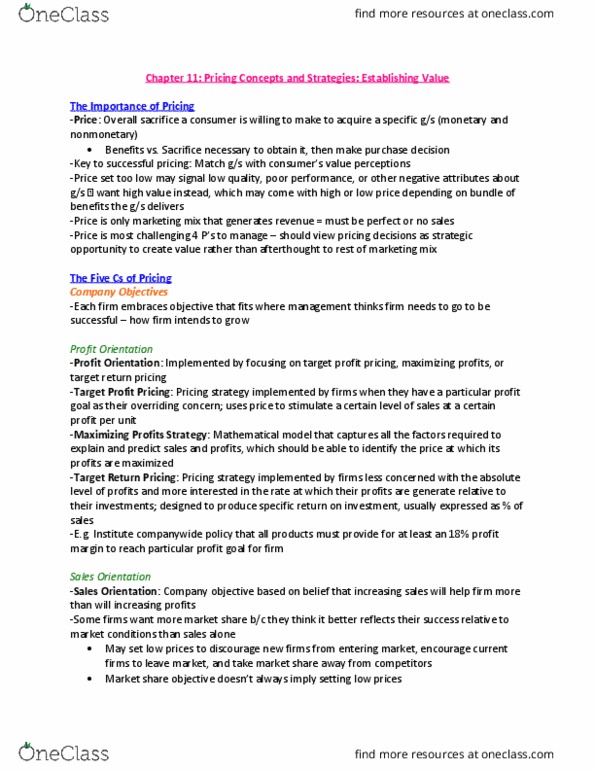

Chapter 11: pricing concepts & strategies: establishing value its of product against sacrifices to obtain it. Price the overall sacrifice a consumer is willing to make money, time, energy to acquire a specific p/s. Key to successful pricing is matching the p/s with consumer"s value perceptions. A low price may trigger thoughts of low quality, poor performance, or other negative attributes. Consumers rank price as one of the most important factors in their purchase decisions. Successful pricing strategies are built through five critical components: Each firm has different objectives & so has to choose a price that fits to be successful. Sales orientation: belief that increasing sales will help the firm more than will increasing profits; taking or holding onto larger market share is the perspective. Competitor orientation: measure themselves mainly against their competition, competitive parity setting prices that are similar to those of major competitors.