BU353 Chapter Notes - Chapter 4: Ex-Ante, Central Limit Theorem, Standard Deviation

Document Summary

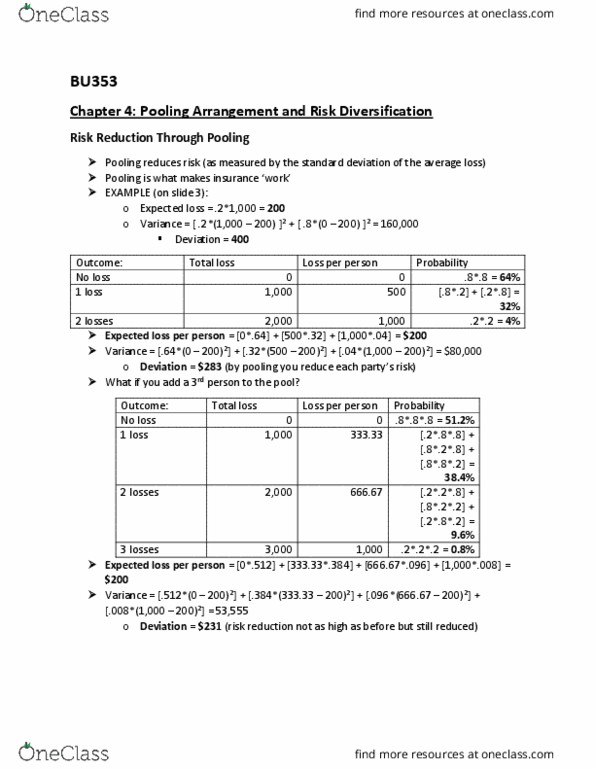

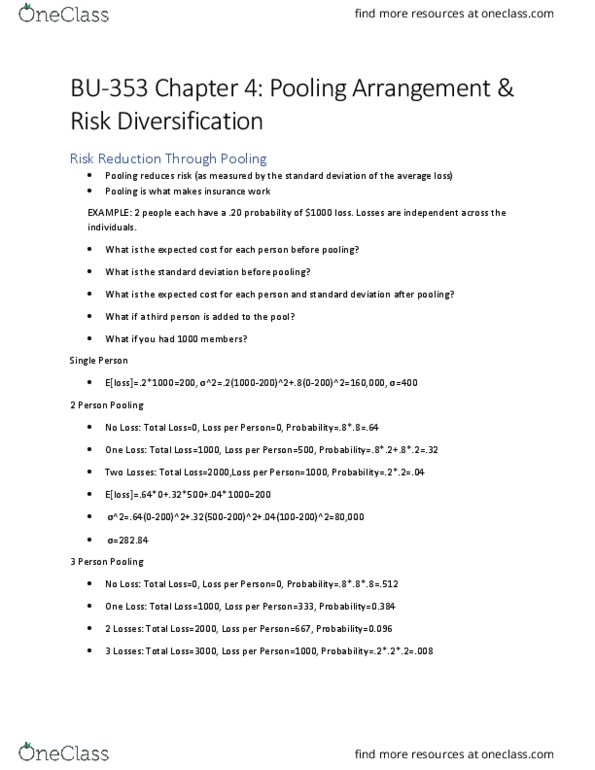

Diversification is an essential aspect of insurance and financial markets. This involves two people and they agree to share losses equally, each paying the average loss. This is referred to as a pooling arrangement, because the two are pooling their resources together to pay the accident costs that my occur. The cost paid by each person is the average loss of the two people. When flipping two coins, the result of flipping the second coin is independent of the first coin. Given the accidents are independent, the probability that both samantha and emily will have an accident is lower than the probability that only emily (or samantha) will have an accident. Because the pooling arrangement reduces the probabilities of the extreme outcomes, the standard deviation (risk) of accident costs paid by both emily and samantha is reduced. The pooling arrangement does not change either person"s expected cost, but it reduces the standard deviation.