BU357 Chapter Notes - Chapter 3: Disability Insurance, Term Life Insurance, Life Insurance

Document Summary

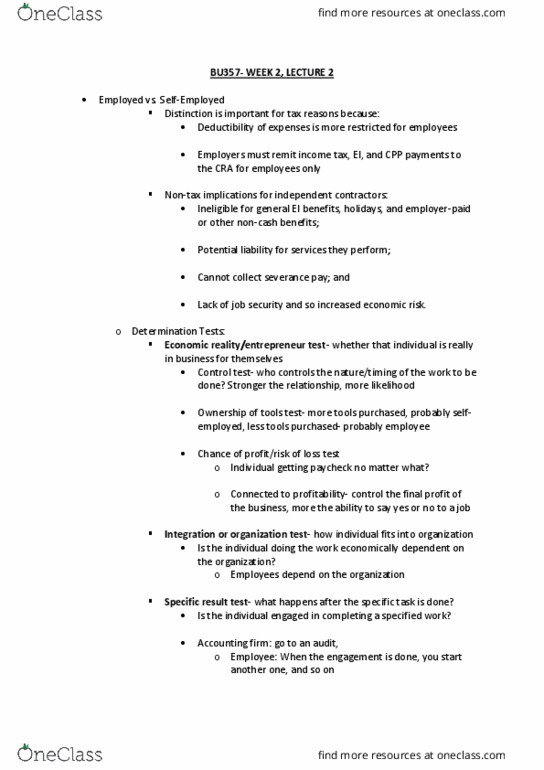

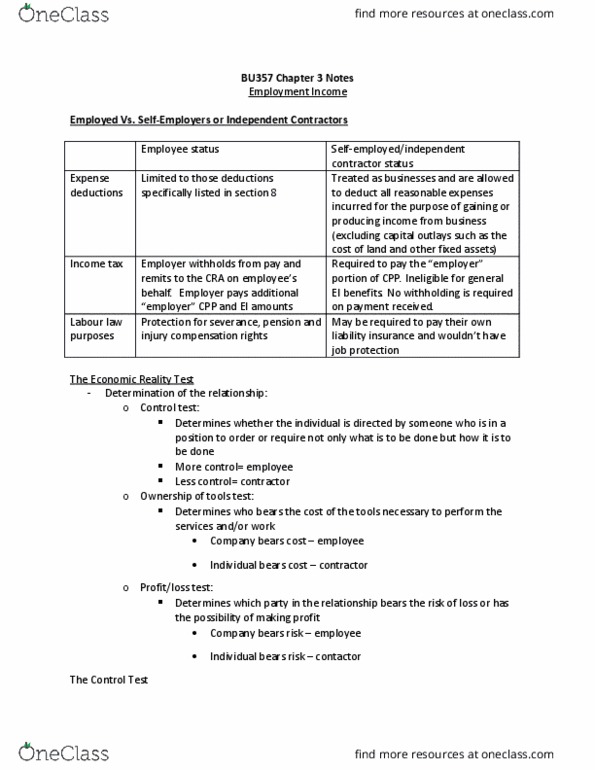

Chapter three - employment income (div b, subd a, s5-8) As per s4, the taxpayer must compute income from each source separately and each source has its own related rules for income inclusions and deductions. A self-employed individual invoices the other party to the contract for services performed and has no source deductions withheld from their remuneration. The potential employer is required to make this determination, though they may request assistance from cra. Cra holds the employer responsible and on audit, can force the employer to make up any shortage in employee and employer portions of required source deductions (ei, cpp & income tax) should they incorrectly assess the relationship. Common law tests are applied in assessing a relationship between the potential employee and the potential employer : Control: an employer usually exercises significant control over what work is performed by an employee and how it is performed.