BU387 Chapter Notes - Chapter 1-12: Comprehensive Income, Current Asset, Measurement Uncertainty

Document Summary

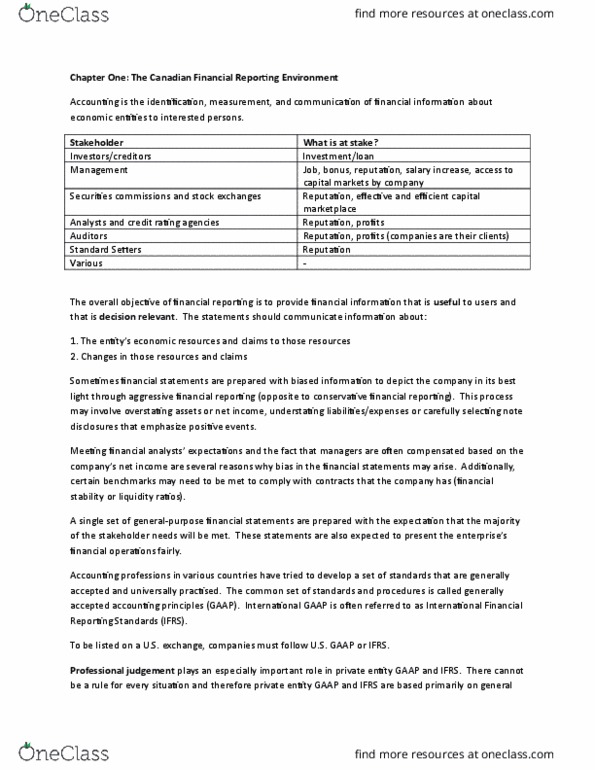

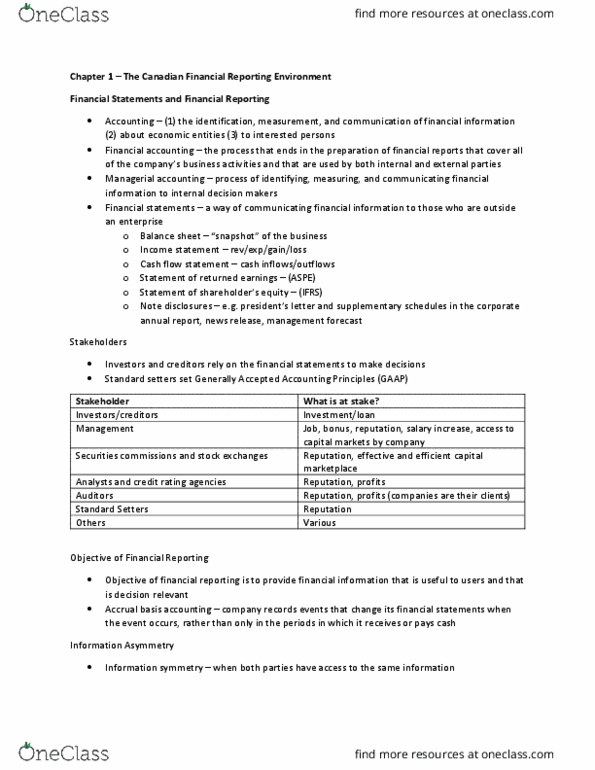

Accounting is the identification, measurement, and communication of financial information about economic entities to interested persons. Job, bonus, reputation, salary increase, access to capital markets by company. The overall objective of financial reporting is to provide financial information that is useful to users and that is decision relevant. The statements should communicate information about: the entity"s economic resources and claims to those resources, changes in those resources and claims. Sometimes financial statements are prepared with biased information to depict the company in its best light through aggressive financial reporting (opposite to conservative financial reporting). This process may involve overstating assets or net income, understating liabilities/expenses or carefully selecting note disclosures that emphasize positive events. Meeting financial analysts" expectations and the fact that managers are often compensated based on the company"s net income are several reasons why bias in the financial statements may arise.