BU397 Chapter Notes - Chapter 15: Subledger, Net Income, Current Asset

Document Summary

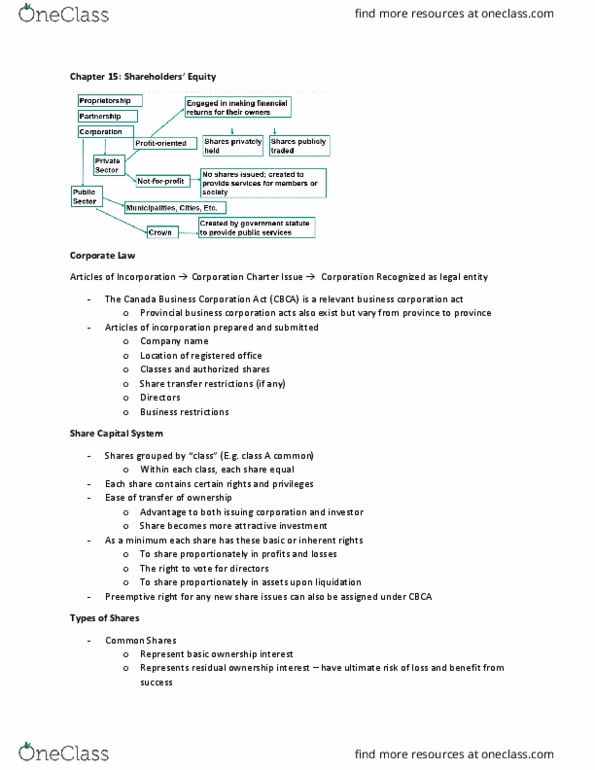

Legal capital (stated capital: the full price received for shares issued. Previously, par value shares were valued at par not what was paid for them. This is no longer allowed under the cbca: authorized capital is the maximum number of shares a company can issue based on the articles of incorporation, issued shares are the number of shares a company has issued. Ifrs: equity is the residual interest in the assets of the entity after deducting all of the liabilities, includes. All undistributed income that remains invested in the business. Cumulative change in equity due to revenues and expenses, and gains and losses from transactions not included in net income: contributed capital is share capital and contributed surplus, earned capital is comprehensive income and retained earnings. There are three important characteristics that impact accounting: corporate law. Any company that wants to establish a corporation must submit articles of incorporation to the government.