BU466 Chapter 14: Chapter 14

Chapter 14 – Rights and Obligations Under the Income Tax Act

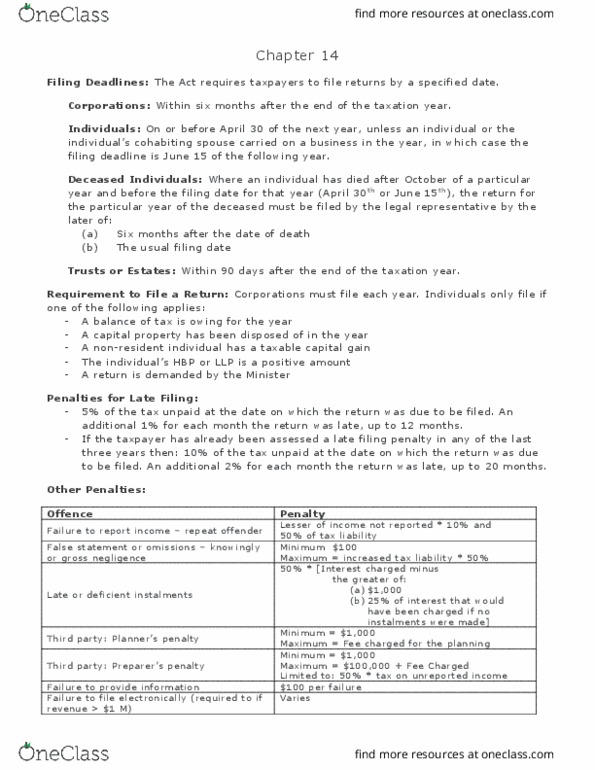

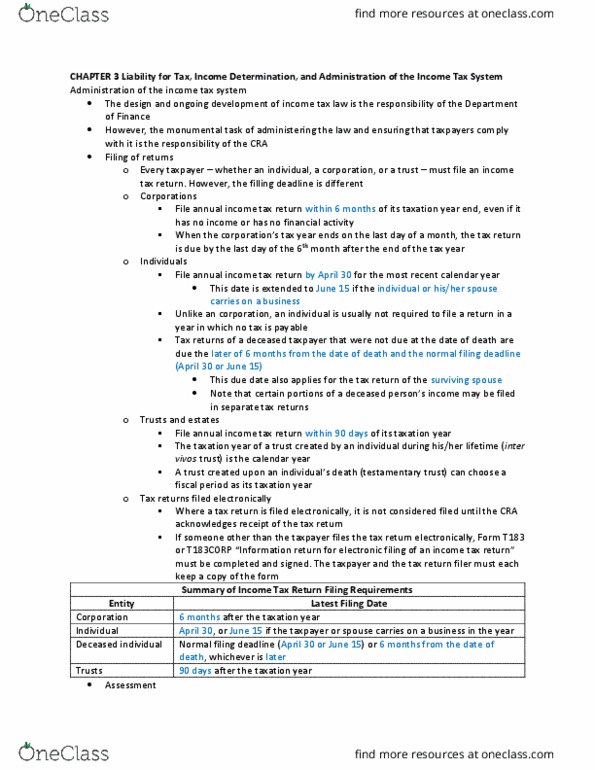

Filing Deadlines

• Corporations – must file within six months after the end of the taxation year

• Individuals - must file on or before April 30, unless idividual’s spouse has a business in the year

then it is June 15

• Deceased individuals – died after October or before filing date (April 30th or June 15th), must be

filed by the later of:

o Six months after the date of death, or

o The usual filing date (April 30th or June 15th)

• Trusts or estates – within 90 days after the end of the taxation year

Requirements to File a Return for Individuals

• Only required to file if one of the following applies:

• A balance of tax is owing for the year

• A capital property has been disposed of in the year

• Non-resident individual has a taxable capital gain

• Idividual’s hoe uyer pla alae or lifelog learig pla is a positive aout

• A return is demanded by the minister

• Individuals benefit from filing if refund due, entitled to GST credit, Canada Child Tax Benefit, OAS

GIS

Electronic and Other Filing Options

• Corporations with annual gross revenues of $1 million or more are required to file their income

tax returns electronically, there are penalties for non-compliance

Failure to File Return

• Balance of tax owing * (5% + 1% per complete month outstanding) to a maximum of 17% of tax

owing

• Repeat offence – penalty above doubled to maximum of 50% of tax owing

Failure to Report Income

• Penalty only if the unreported income and any of the three prior years was equal to or greater

than $500

• Lesser of 10% of income omitted or 50% of understated unpaid taxes

False Statements or Omission

• Penalty equal to the greater of $100 and 50% of the difference in tax liability

• Must be gross negligence – which include errors which amount to little more than careless

omissions

Interplay of Penalty Provisions

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

Chapter 14 rights and obligations under the income tax act. Filing deadlines: corporations must file within six months after the end of the taxation year. I(cid:374)dividual"s ho(cid:373)e (cid:271)uyer pla(cid:374) (cid:271)ala(cid:374)(cid:272)e or lifelo(cid:374)g lear(cid:374)i(cid:374)g pla(cid:374) is a positive a(cid:373)ou(cid:374)t. Individuals benefit from filing if refund due, entitled to gst credit, canada child tax benefit, oas. Electronic and other filing options: corporations with annual gross revenues of million or more are required to file their income tax returns electronically, there are penalties for non-compliance. Failure to file return: balance of tax owing * (5% + 1% per complete month outstanding) to a maximum of 17% of tax owing, repeat offence penalty above doubled to maximum of 50% of tax owing. Failure to report income: penalty only if the unreported income and any of the three prior years was equal to or greater than . Lesser of 10% of income omitted or 50% of understated unpaid taxes.