BU477 Chapter Notes - Chapter 7: Risk Measure, Disaster Recovery Plan, Change Detection

Document Summary

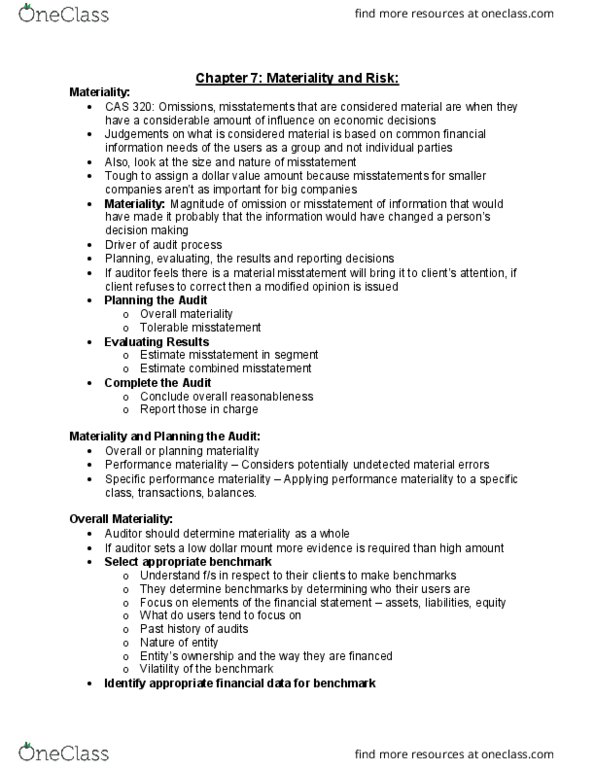

Misstatements (inc. omissions) are material if they individually or in the aggregate could reasonably be expected to influence the economic decisions of users taken on the basis of the f/s. Judgments are made in light of circumstances surrounding the entity and are affected by the size and nature of the misstatement, or combination of both. Judgments about what is material to users of the f/s are based on consideration of the common financial information needs of users as a group, not each user individually. Materiality is driver of entire audit process planning, evaluating results, and reporting decisions. First 3 decisions made in planning stage form benchmarks to evaluate results of audit testing, to make conclusions (on f/s, accounts, and disclosures), and to complete the audit (issuing audit report, reporting to execs) Material misstatement = bring to client"s attention so correction can be made. If client refuses to correct statements, modified opinion must be issued.