BU477 Chapter Notes - Chapter 2: Sole Proprietorship, Public Company Accounting Oversight Board, Risk Management

Document Summary

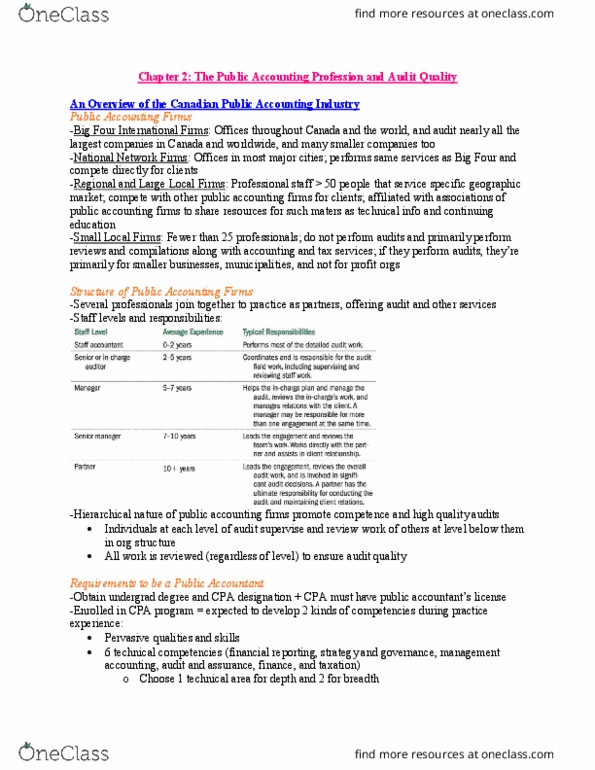

Big four international: they have offices throughout canada and the world: deloitte, pwc, kpmg, ey. National: have offices in the major cities and perform the same things as international but are much smaller: grant thornton, mnp, bdo, collins barrow. Regional and local firms: fewer than 50 public accounting firms in this category. Some of these firms only have one office and serve close clients: richtner, mallette, hlb, crowe mackay. Small local firms: fewer than 25 professionals in a single office and do not perform audits. Generally, are limited liability only liable for the amount you have contributed. Hierarch consist of partners, managers, supervisor, senior, staff accountant. Manager and partner will review the staff accountants work. Must choose one technical area of depth and two areas of breadth. To be a public accountant but choose assurance as depth. Cpa canada: represents cpa profession nationally and internationally.