BU477 Chapter Notes - Chapter 4: Confirmation Bias, Ethical Decision, Financial Statement

Document Summary

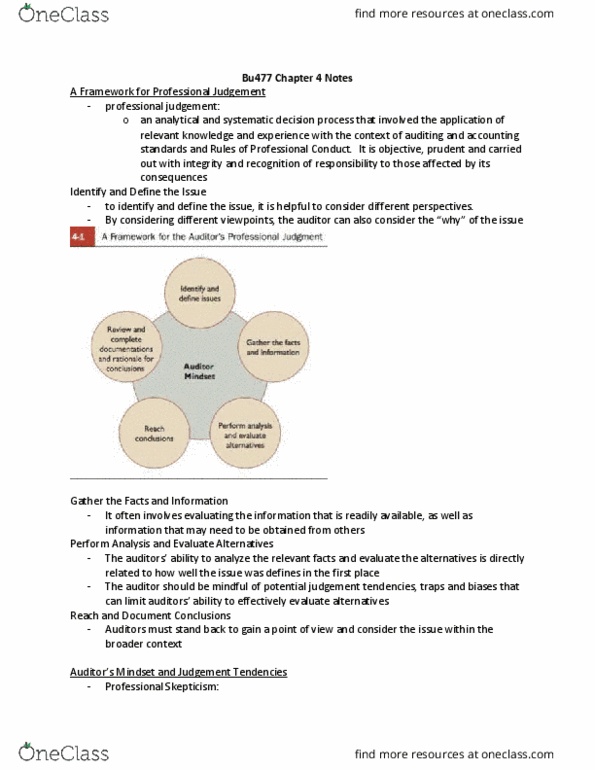

Application of relevant knowledge and experience within context of providing auditing and accounting opinions. Professional judgement: analytical and systematic, objective prudent and carried out with integrity and recognition of responsibility to those affected by its consequence: making the right judgement and providing your duty of care in auditing opinions. Must prove that decision is: well thought out, objective, meets gaap and gaas, evidence to support decision, maximize likelihood of good consequence, carried out truthfulness and forthrightness, considers impact on financial statement users. Frameworks help guide thinking and encourage auditors to be aware of judgement bias. We must clear about what we want to solve because we don"t want to solve the wrong problem. Try to take on different perspectives to determine the real issue. Can also determine why the issue is there when approaching multiple viewpoints. Also, avoids judgement trap in jumping/rushing to solve the problem. Often evaluating the information that is readily available for auditors.