BU487 Chapter Notes - Chapter 6: Equity Method, Retained Earnings, Historical Cost

Document Summary

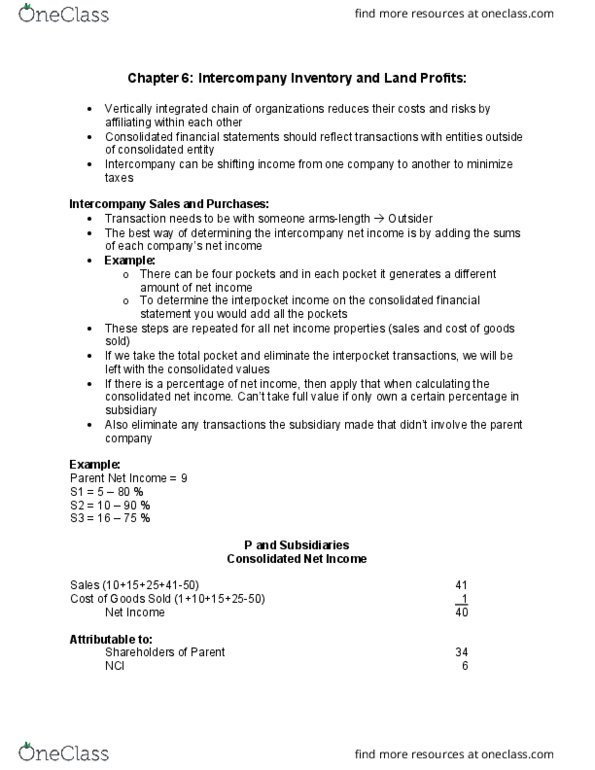

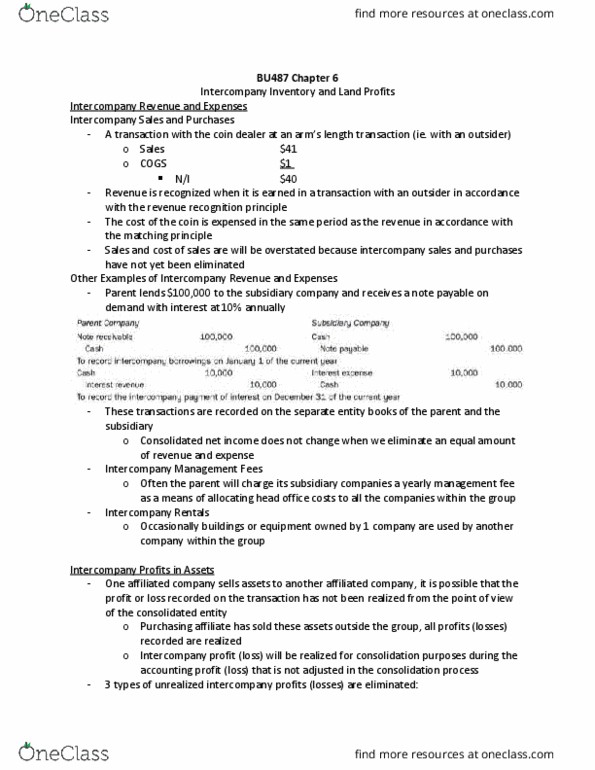

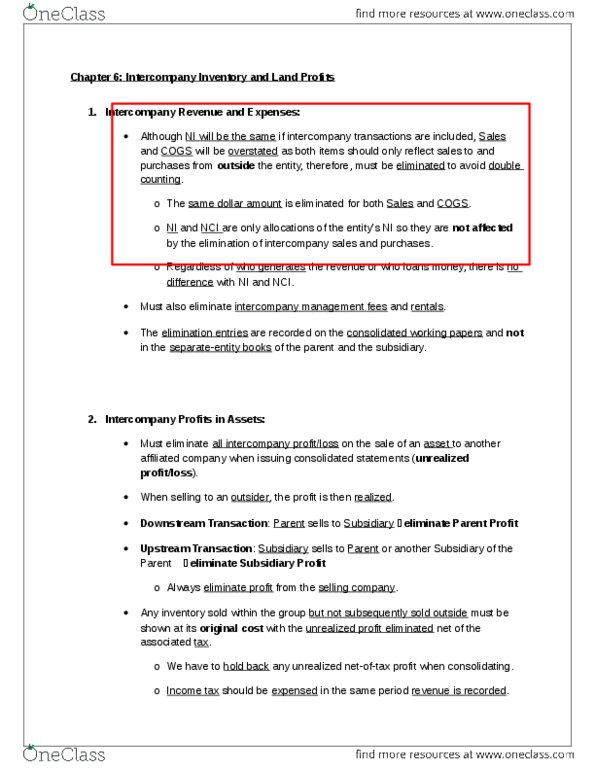

Bu 487 advanced acctg, kyle somerville: consolidated financial statements should reflect only transactions with entities outside of the. Chapter 6: intercompany inventory and land profits consolidate entity. Intercompany sales and purchases: a(cid:396)(cid:373)"s le(cid:374)gth t(cid:396)a(cid:374)sa(cid:272)tio(cid:374) with an outsider, both sales and cost of goods sold should only reflect sales to and purchases from outside the entity, eg. Rare coin sales between pockets and an outsider end with same net income but sales and cost of goods sold will be higher if recording the interco transactions. Non-controlling interest = (therefore total is the net income from first example) Just an exchange of cash but no revenue or expense should be recognized: eg. Note receivable and interest revenue vs. interest expense. Intercompany management fees: must be eliminated from consolidated income statements, the parent may charge the subsidiary for allocating head office costs but no actual revenue or expense should be recognized.