EC223 Chapter Notes - Chapter 17: Excess Reserves, Pras, Quantitative Easing

Document Summary

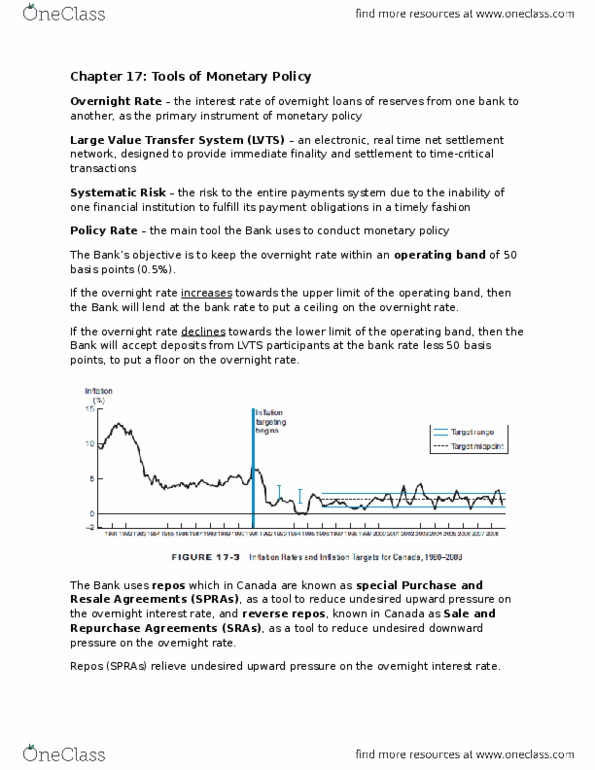

Overnight rate the interest rate on overnight loans of reserves from one bank to another, as the primary instrument of monetary policy. The framework for the implementation of monetary policy. The tools used by the bank of canada to implement monetary policy are closely linked to the institutional arrangements regarding the clearing and settlement systems in the canadian economy. An electronic, real-time net settlement network, designed to provide immediate finality and settlement to time-critical transactions. In addition to the bank of canada, there are 14 lvts participants. The lvts has been put into place in order to eliminate systematic risk the risk to the entire payments system due to the inability of one financial institution to fulfill its payment obligations in a timely fashion. Each lvts payment is subject to real time risk-control tests to confirm that sufficient collateral is available, and is final and irrevocable in real time. Participants know in real time their large-value, wholesale transactions.