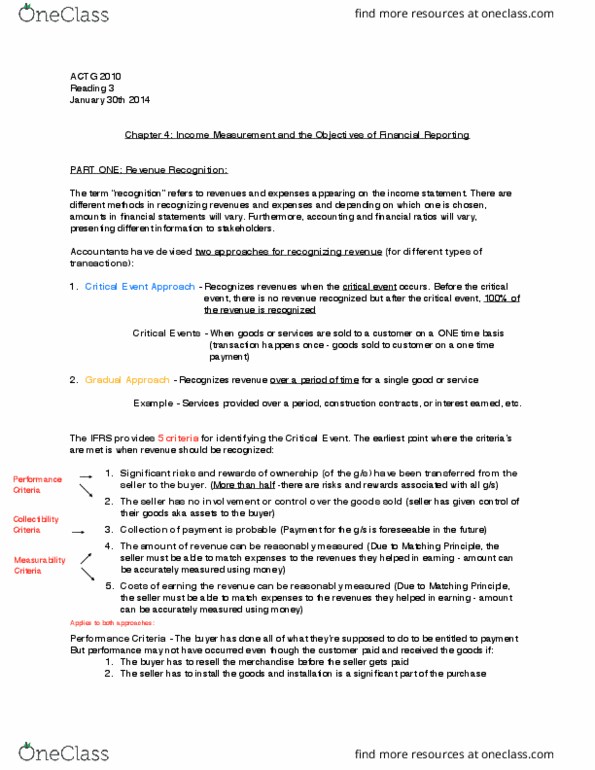

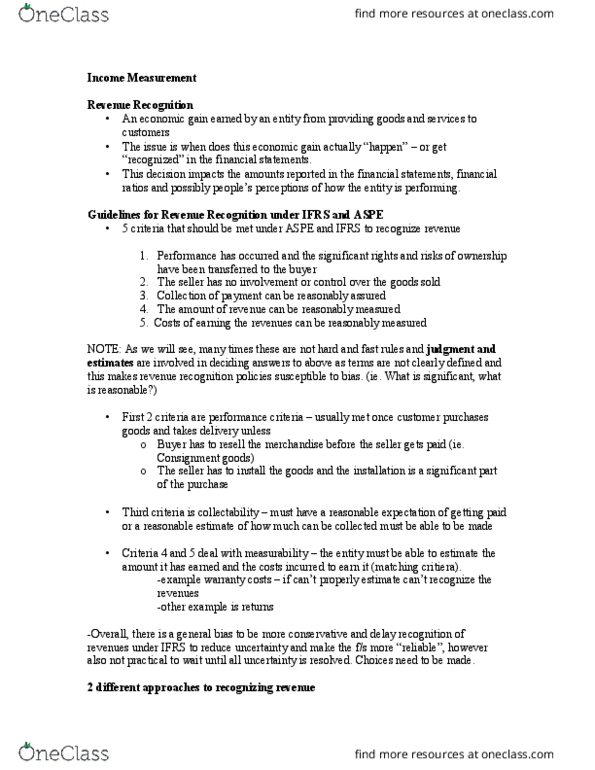

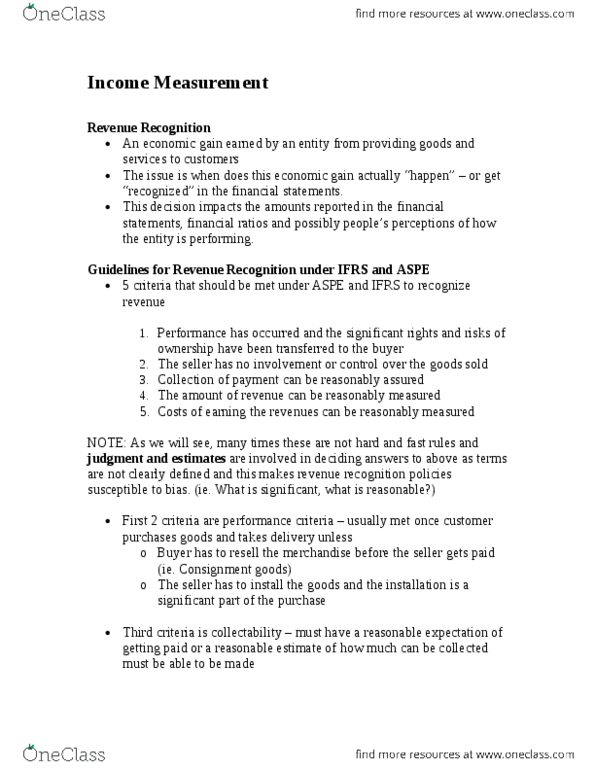

ACTG 2010 Chapter 4: Chapter 4 Notes.docx

Document Summary

Get access

Related Documents

Related Questions

Identify two categories of revenue for Panera Bread from the table in the article Revenue Recognition: Key differences between U.S. GAAP and IFRSs. Compare and contrast the companyâs current U.S. GAAP revenue recognition with the potential adoption of IFRS. Provide the IASB Framework or the IAS statement, the changes in revenue recognition as well as potential challenges the company may face in adoption.

Table:

| Subject | U.S. GAAP | IFRSs |

|---|---|---|

| Concept/objective | realized or realizable and earned. | According to paragraph 83 of the IASB's Framework for the Preparation and Presentation of Financial Statements, revenue is recognized when (1) "it is probable that any future economic benefit" will flow to the entity and (2) such a benefit can be measured reliably. Further, paragraph 93 of the IASB Framework indicates that revenue normally must be earned before it can be recognized. |

| Definition of revenue | Paragraph 78 of FASB Concepts Statement No. 6, Elements of Financial Statements, defines revenue as "inflows or other enhancements of assets of an entity or settlements of its liabilities (or a combination of both) from delivering or producing goods, rendering services, or other activities that constitute the entity's ongoing major or central operations." | Paragraph 74 of the IASB Framework states, "The definition of income encompasses both revenue and gains. Revenue arises in the course of the ordinary activities of an entity and is referred to by a variety of different names including sales, fees, interest, dividends, royalties and rent." Paragraph 7 of IAS 18 defines revenue as "the gross inflow of economic benefits during the period arising in the course of the ordinary activities of an entity when those inflows result in increases in equity, other than increases relating to contributions from equity participants." |

| Sale of goods or products | SAB Topic 13 indicates that revenue from the sale of goods or products should not be recognized until it is earned and realized, or realizable. Revenue is generally earned and realized, or realizable, when all of the following conditions have been satisfied: There is persuasive evidence of an arrangement. Delivery has occurred (e.g., an exchange has taken place). The sales price is fixed or determinable. Collectibility is reasonably assured. In addition, ASC 605-15 provides guidance on product transactions that include a right of return. Further, various industry- and transaction-specific guidance is provided in other U.S. GAAP. | Under paragraph 14 of IAS 18, revenue from the sale of goods is recognized if all of the following conditions are met: The "entity has transferred to the buyer the significant risks and rewards of ownership of the goods." The "entity retains neither continuing managerial involvement to the degree usually associated with ownership nor effective control over the goods sold." The "amount of revenue can be measured reliably." "[I]t is probable that the economic benefits associated with the transaction will flow to the entity." The "costs incurred or to be incurred in respect of the transaction can be measured reliably." |

| Rendering services | >Like revenue from product sales, revenue from service transactions should not be recognized until it is earned and realized, or realizable. Revenue is generally earned and realized, or realizable, when all of the following conditions have been satisfied: There is persuasive evidence of an arrangement. Service has been rendered. The sales price is fixed or determinable. Collectibility is reasonably assured. Other than the limited guidance in >ASC 605-20, no specific guidance on the rendering of services exists under U.S. GAAP. The appropriate method for recognizing revenue in such transactions depends on the individual transaction but is usually based on the proportional performance as of the balance sheet date. | Paragraph 20 of IAS 18 states, "When the outcome of a transaction involving the rendering of services can be estimated reliably, revenue associated with the transaction shall be recognised by reference to the stage [i.e., percentage] of completion of the transaction at the balance sheet date." Paragraph 20 goes on to list specific conditions for determining whether an outcome of a transaction can be estimated reliably. And subsequent paragraphs provide guidance on determining the stage of completion. Paragraph 26 of IAS 18 states, "When the outcome of the transaction involving the rendering of services cannot be estimated reliably, revenue shall be recognised only to the extent of the expenses recognised that are recoverable." |

| Software arrangements | ASC 985-605 provides guidance on recognizing revenue in a software arrangement. | There is no specific guidance on software revenue recognition in IFRSs. An entity should apply the provisions of IAS 18 as appropriate. |

| Construction-type contracts | ASC 605-35 provides guidance on construction-type contracts. ASC 605-35-25-90 indicates that when the percentage-of-completion method is deemed inappropriate (e.g., when dependable estimates cause the outcome to be doubtful), the completed-contract method is preferable. ASC 605-35-25-25 through 25-27, the customer must approve the scope and price of change orders before the related revenue can be recognized. | IAS 11, Construction Contracts, provides guidance on construction-type contracts. Paragraph 32 of IAS 11 indicates that when the percentage-of-completion method is deemed inappropriate (e.g., when the outcome of the contract cannot be estimated reliably), revenue is recognized to the extent that costs have been incurred, provided that the costs are recoverable. Use of the completed-contract method is prohibited under IFRSs. Paragraph 13 of IAS 11 specifies that when it is probable that the customer will approve the scope and price of a change order, the related revenue can be recognized. |

| Milestone method | ASC 605-28 provides guidance on the application of the milestone method for recognizing revenue in research or development arrangements. | There is no specific guidance in IFRSs on the application of the milestone method for recognizing revenue in research or development arrangements. |

| Multiple-element arrangements | ASC 605-25 provides guidance on multiple-element revenue arrangements and establishes detailed criteria for determining whether each element may be separately considered for recognition. This guidance does not apply to arrangements or deliverables that are within the scope of other authoritative literature (e.g., ASC 985-605). | Paragraph 13 of IAS 18 indicates that the recognition criteria under IAS 18 are usually applied separately to each transaction unless either of the following conditions applies: "[I]t is necessary to apply the recognition criteria to the separately identifiable components of a single transaction in order to reflect the substance of the transaction." Two or more transactions "are linked in such a way that the commercial effect cannot be understood without reference to the series of transactions as a whole." |

| Bill-and-hold arrangements | The SEC staff lists specific criteria that must be met for revenue to be recognized in bill-and-hold arrangements before delivery of the product. (Non-SEC entities also use these revenue recognition criteria because no other authoritative guidance in U.S. GAAP addresses the accounting for these transactions.) The criteria restrict revenue recognition to limited circumstances. | Illustrative Examples to IAS 18 list criteria for recognizing revenue under bill-and-hold arrangements before delivery of the product. While the objective for recognizing revenue in bill-and-hold arrangements may be similar to that in U.S. GAAP, the criteria are not the same. |

| Gross versus net | ASC 605-45 provides guidance on whether to report revenue on the basis of the gross amount billed to the customer (as a principal) or the net amount retained by the company (as an agent). | Paragraph 8 of IAS 18 requires that revenue be reported on a net basis in agency relationships but does not provide specific guidance to consider. Improvements to IFRSs issued in April 2009) provides examples that indicate whether an entity is acting as a principal or as an agent. |

| Customer loyalty programs | Revenue recognition for customer loyalty programs is not specifically addressed in U.S. GAAP. (The EITF attempted to address this issue but did not reach a consensus.) Although entities account for customer loyalty programs in different ways, such programs are typically accounted for under ASC 605-25 as multiple-element arrangements or under an incremental-cost model. | IFRIC 13 indicates that customer loyalty programs are deemed multiple-element revenue transactions and that the fair value of the consideration received should be allocated between the components of the arrangement. |

| Rebates, discounts, incentives, and other consideration | ASC 605-50 indicates that consideration given by an entity to its customers is presumed to be a reduction of revenue unless an identifiable benefit whose fair value can be reasonably estimated is received. | Paragraph 10 of IAS 18 states that revenue "is measured at the fair value of the consideration received or receivable taking into account the amount of any trade discounts and volume rebates allowed by the entity." There is no specific guidance on other types of consideration given by an entity to its customers. |

| Specific industry and other guidance | Certain standards in U.S. GAAP provide specialized guidance on revenue recognition, including guidance that applies to specific industries and transactions. | IFRSs provide no (or limited) revenue recognition guidance that applies to specific industries or transactions. |

Question 1

Identify the item below that is not one of the four different types of data processing activities.

| deleting | ||

| reading | ||

| creating | ||

| using |

Question 2

All of the following are advantages of an ERP system except

| ERPs permit manufacturing plants to receive new orders in real time. | ||

| in an ERP, data input is captured or keyed once. | ||

| it takes considerable experience and training to use an ERP system effectively. | ||

| ERPs permit management to gain greater visibility into every area of the enterprise. |

Question 3

Sam Jones has been the controller of Downtown Tires for 25 years. Ownership of the firm recently changed hands and the new owners are conducting an audit of the financial records. The audit has been unable to reproduce financial reports that were prepared by Sam. While there is no evidence of wrongdoing, the auditors are concerned that the discrepancies might contribute to poor decisions. Which of the following characteristics of useful information is absent in the situation described above?

| relevant | ||

| reliable | ||

| complete | ||

| timely | ||

| understandable | ||

| verifiable | ||

| accessible |

Question 4

An ERP system might facilitate the purchase of direct materials by all of the following except

| preparing a purchase order when inventory falls to reorder point. | ||

| routing a purchase order to a purchasing agent for approval. | ||

| communicating a purchase order to a supplier. | ||

| selecting the best supplier by comparing bids. |

Question 5

Antia Carmie is the largest collector and retailer of Japanese fans in the St. Louis area. Antia uses computer technology to provide superior customer service. The store's database system was designed to make detailed information about each Japanese fan easily accessible to her customers. Accordingly, the fan price and condition are provided for each fan, along with many pictures of each fan. In Antia's database, the price of the Japanese fans is a(n)

| entity. | ||

| attribute. | ||

| field. | ||

| record. |

Question 6

Which of the following is not considered a source document?

| A copy of the company's shipping document. | ||

| A copy of the company's ledger. | ||

| A copy of the company's sales journal. | ||

| A copy of the company's financial statements. |

Question 7

In an ERP system, the module used to record data about transactions in the disbursement cycle is called

| financial. | ||

| order to cash. | ||

| customer relationship management. | ||

| purchase to pay. |

Question 8

Baggins Incorporated identifies new product development and product improvement as the top corporate goals. An employee developed an innovation that will correct a shortcoming in one of the company's products. Although Baggins current Return on Investment (ROI) is 12%, the product innovation is expected to generate ROI of only 10%. As a result, awarding bonuses to employees based on ROI resulted in

| goal conflict. | ||

| information overload. | ||

| decreased value of information. | ||

| goal congruence. |

Question 9

________ are examples of activities that constitute inbound logistics.

| Activities that transform inputs into final products or services | ||

| Activities that provide post-sale support to customers | ||

| Activities that consist of receiving, storing, and distributing the materials used as inputs by the organization to create goods and/or services it sells | ||

| Activities that help customers to buy the organization's products or services |

Question 10

In which transaction cycle would information for inventory purchases be most likely to pass between internal and external accounting information systems?

| the revenue cycle | ||

| the expenditure cycle | ||

| the human resources / payroll cycle | ||

| the financing cycle |

Question 11

The collection of customer payment is part of which transaction cycle?

| the human resources cycle | ||

| the production cycle | ||

| the revenue cycle | ||

| the expenditure cycle |

Question 12

Which of the following is an example of source data automation?

| POS (point-of-sale) scanners in retail stores | ||

| a bill of lading | ||

| a subsidiary ledger | ||

| a utility bill |

Question 13

All of the following are guidelines for developing a good coding system except

| be as sophisticated as possible to promote usage. | ||

| be consistent with its intended use. | ||

| be flexible to allow for growth. | ||

| be consistent with the company's organization structure. |

Question 14

What is a key decision that needs to be made with regards to borrowing money from lenders?

| the location | ||

| pro forma income statement | ||

| how much capital to acquire | ||

| job descriptions |

Question 15

Identify the false statement below.

| A service company does not have an inventory system. | ||

| Retail stores do not have a production cycle. | ||

| Financial institutions have installment-loan cycles. | ||

| Every organization should implement every transaction cycle module. |

Question 16

The chart of accounts of a fast-food restaurant would probably include

| a list of customers. | ||

| a list of financial statement accounts. | ||

| a list of vendors. | ||

| a list of employees. |

Question 17

Which statement below regarding the AIS is false?

| Traditionally, most AIS have been designed so that both financial and operational data are stored in a manner that facilitates their integration in reports. | ||

| The AIS must be able to provide managers with detailed and operational information about the organization's performance. | ||

| Both traditional financial measures and operational data are required for proper and complete evaluation of performance. | ||

| The AIS was often just one of the information systems used by an organization to collect and process financial and nonfinancial data. |

Question 18

In Petaluma, California, electric power is provided to consumers by Pacific Power. Each month Pacific Power mails bills to 186,000 households and then processes payments as they are received. What is the best way for this business to ensure that payment data entry is efficient and accurate?

| well-designed paper forms | ||

| turnaround documents | ||

| source data automation | ||

| sequentially numbered bills |

Question 19

Data must be converted into information to be considered useful and meaningful for decision making. There are seven characteristics that make information both useful and meaningful. If the same information can be reproduced by two independent and knowledgeable people, it is representative of the characteristic of

| verifiability. | ||

| truthful. | ||

| relevance. | ||

| reliability. |

Question 20

Antia Carmie is the largest collector and retailer of Japanese fans in the St. Louis area. Antia uses computer technology to provide superior customer service. The store's database system was designed to make detailed information about each Japanese fan easily accessible to her customers. Accordingly, the fan price and condition are provided for each fan, along with many pictures of each fan. In Antia's database, the data about each Japanese fan represents a(n)

| entity. | ||

| attribute. | ||

| field. | ||

| record. |