ACTG 2020 Chapter Notes - Chapter 10: Cost Driver, Fixed Cost, Deutsche Luft Hansa

9 Dec 2013

School

Department

Course

Professor

Document Summary

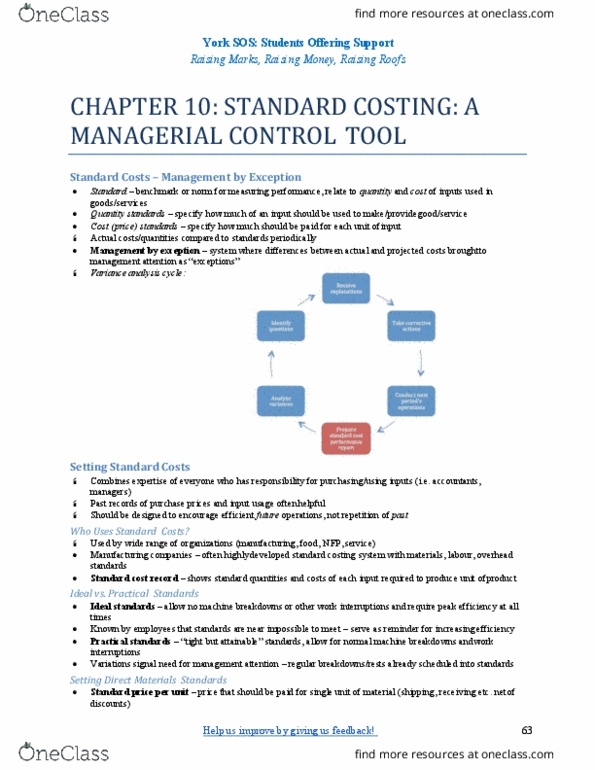

Chapter 10 standard costs and overhead analysis. Standard a benchmark or a norm for measuring performance. Standards are widely use in managerial accounting where they relate to quantity and cost of inputs used in manufacturing goods or producing services. Quantity and cost standards are set for major input (raw materials, labour time) Quantity standards specify how much of an input should be used to make unit of a product or provide a unit of service. Cost (price) standards specify how much should be paid for each unit of the input. Variances occur when there are discrepancies things don"t meet standards. Standards should be designed to encourage efficient future operations, not a repetition of past operations that may or may not have been efficient. Practical standards standards that allow for normal machine downtime and other work interruptions and can be attained through reasonable, although highly efficient, efforts by the average employee; tight but attainable standards our focus for the chapter.