ACTG 2020 Chapter Notes - Chapter 11: Ginger Beer, Accounts Receivable, Quality Costs

9 Dec 2013

School

Department

Course

Professor

Document Summary

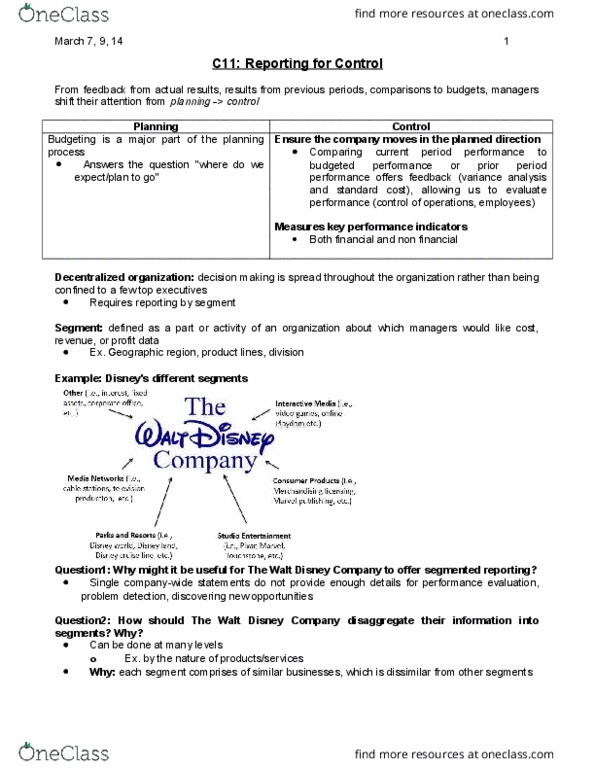

Feedback of actual results, comparison to other orgs, other periods, mgers attempt to ensure orgs moves in planned direction -> performance assessment or control. Segment reporting, responsibility centre reporting, investment performance, and profitability analysis are four commonly used reporting structures that provide somewhat different types of information: each represent a different aspect of organizational control. Increasingly, companies are using non-financial indicators of performance such as scrap levels, rework efforts, market share, employee morale, pollutant discharges, and customer satisfaction. Decentralization in organizations decentralized organization, decision making is spread throughout the organization, rather than. In a being confined to a few top executives. Segment reporting is key for analyzing and evaluating decisions made by segment managers. Need reports for each segment: a segment is defined as a part or activity of an organization about which managers would like cost, revenue, or profit data.