ACTG 2010 Chapter Notes - Chapter 7: Book Value, Internal Control, Write-Off

Document Summary

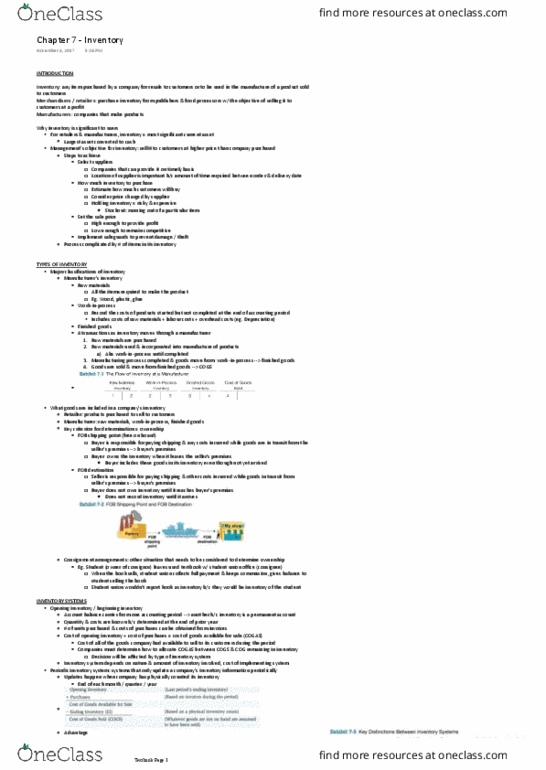

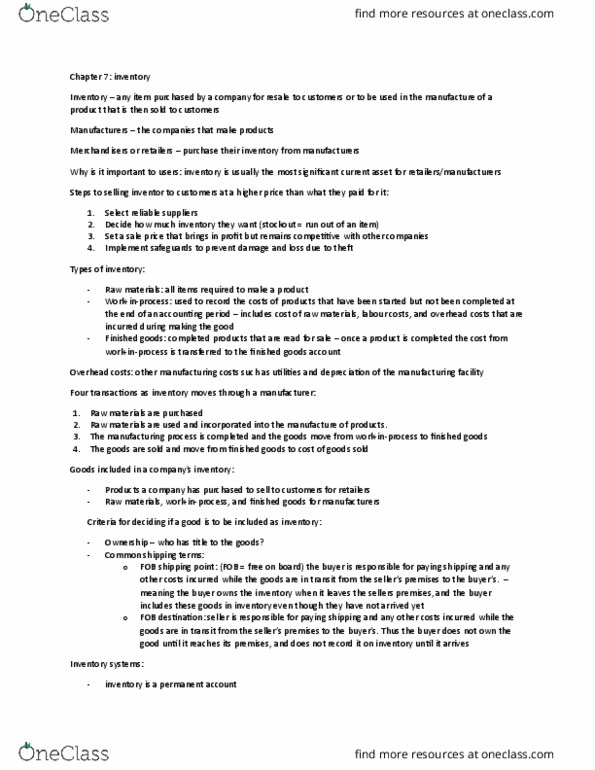

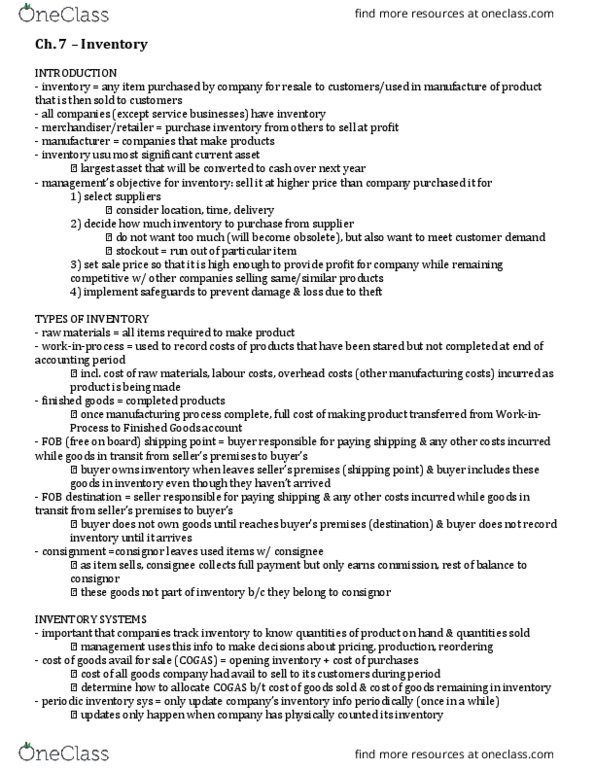

Actg 2010 chapter 7 inventory notes pg. Inventory: any item purchased by the company for resale to customers or to be used to manufacture a product to sell to a customer. Covenant: conditions or restrictions placed on a company that borrows money. Usually require the company maintain certain minimum ratios (1:1 current asset to current. Liabilities) and may restrict its ability to pay dividends. Management must source suppliers, determine order quantities, establish selling prices and implement safeguard to protect against damage and theft. Manufacturers have three classes of inventory: 1. 4 transactions as inventory moves thru manufacturer: 1. Raw materials used in manufacturing dr work in progress inventory cr. Fob shipping point: (cid:271)e(cid:272)o(cid:373)e part of the (cid:271)uyer"s i(cid:374)(cid:448)e(cid:374)tory (cid:449)he(cid:374) they lea(cid:448)e the seller"s premise: buyer pays shipping. Fob destination: become part of inventory when they are received at the (cid:271)uyer"s premise: seller pays shipping.