ACTG 2020 Chapter Notes - Chapter 3: Squared Deviations From The Mean, Scatter Plot, Cost Driver

31 Jan 2017

School

Department

Course

Professor

Document Summary

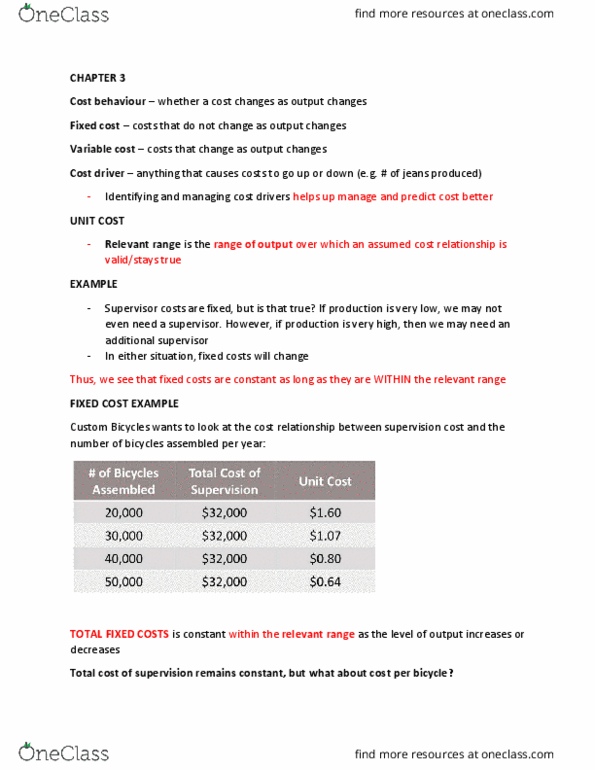

Introduction: costs can be variable, fixed or mixed, costs change to the amount of output produced. In order to know how many products to produce --> need to know the capacity (how much we can produce) and demand (how much we should produce) If company produced a few pairs each year --> would not need a supervisor. If company produced 2 - 3 times more --> need to add more shifts --> cost increases. Variable costs: variable costs - costs that, in total, vary in direct proportion to changes in output within the relevant range, total variable cost = variable rate per unit x amount of output. Stays the same: per-unit fixed cost is not that valuable, unit variable cost is a lot more valuable. Are real-world cost relationships linear: most relationships are not linear, example: increased demand for a certain period of time.