ADMS 3585 Chapter Notes - Chapter 4: Net Income, Income Statement, Current Asset

19 Oct 2012

School

Department

Course

Professor

Document Summary

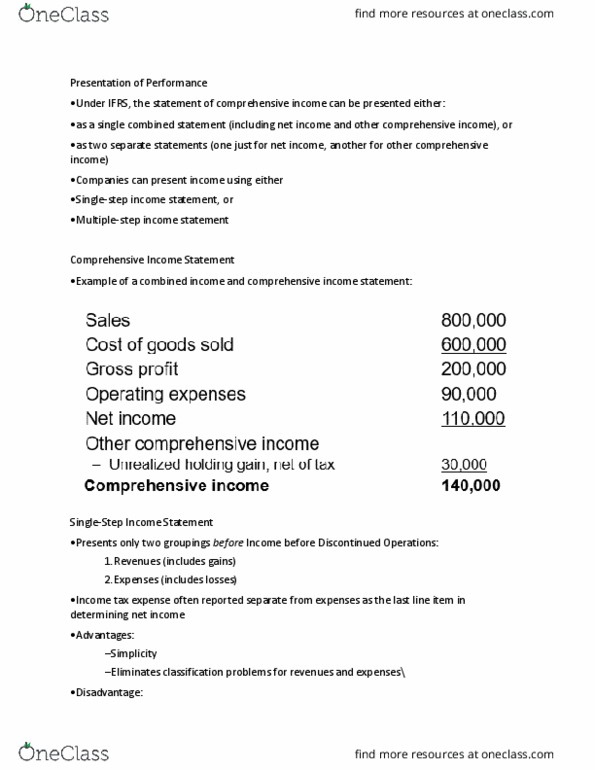

Presenting expenses: nature versus function: under ifrs, analysis of expenses must be presented based on either, nature of expenses, or, function of expenses. If expenses are presented by function, nature of expenses must also be disclosed: no similar requirement under private entity gaap, choice should result in information that is more reliable and relevant. Revenues: net sales, other revenues (e. g. dividend, rental) Selling expenses: cost of goods sold, administrative expenses. Income tax expense: presents only two groupings before income before discontinued operations, revenues (includes gains, expenses (includes losses) Income tax expense often reported separate from expenses as the last line item in determining net income: advantages, simplicity, eliminates classification problems for revenues and expenses, disadvantage, operating and non-operating activities reported together lower relevance. Atypical and material, subject to mgr intention. Gains and losses that do not qualify as an extraordinary item but are material in amount: one of infrequent or atypical and does depend on management decisions.