ADMS 3520 Chapter : Introductory Notes.pdf

23 Apr 2012

School

Department

Course

Professor

Document Summary

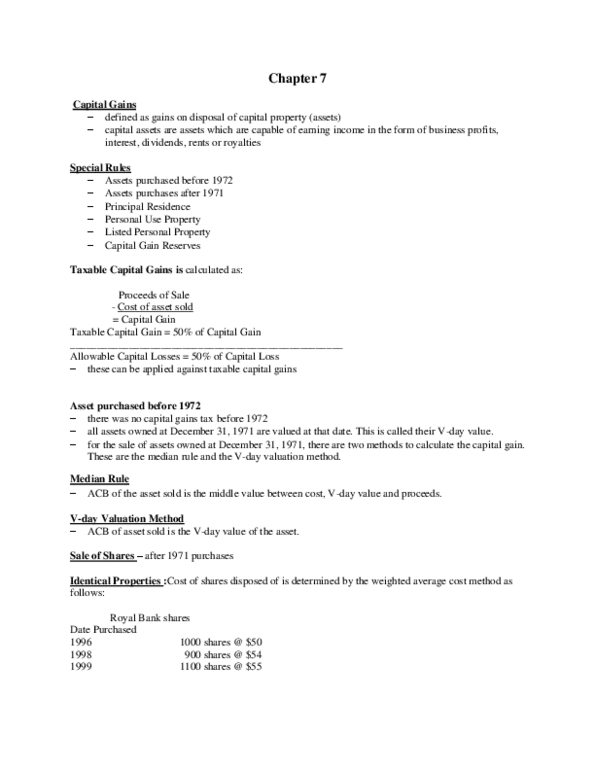

+ taxable capital gains which exceed allowable capital. Salary received + taxable benefits are taxable. Some benefits received from employment are not taxable. There are some deductions allowed against employment income. Income from business ch 4 + ch 5. An income statement is required to be prepared with a year end of december 31 using rules from the income. If there is a loss from a business, it is deductible against other income. Income from an unincorporated business is taxable on the personal tax return. (an incorporated company files a corporate tax return). Capital gains are taxable based on of the gain. Taxable capital gain = (1/2 x 1,100) Allowable capital losses are deductible against taxable capital gains only. Income from the sale of capital property such as stocks, mutual funds or land is taxable. This is investment income: interest, dividends, royalties, rental income. Interest and dividend income is listed on a t-5 slip.