ADMS 3595 Chapter Notes - Chapter 19: Defined Contribution Plan, Defined Benefit Pension Plan, Deferred Compensation

10 Mar 2018

School

Department

Course

Professor

Document Summary

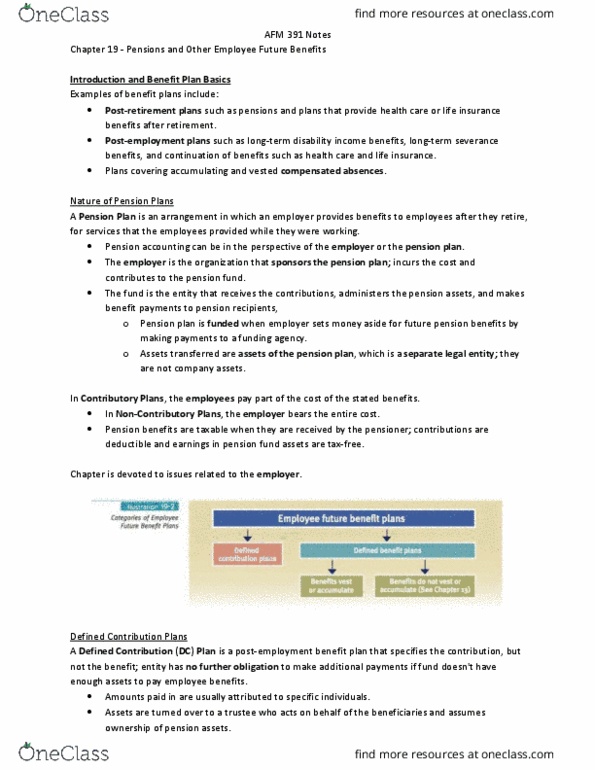

Adms 3595 ch 19 pensions & other post employment benefits. Ifrs remeasurements charged to aoci: employees beneficiaries of defined contribution trust, employer beneficiary of defined benefit trust, trust in form trust = separate entity. Focus more on current salary level: changes in defined benefit obligations, dbo actuarial pv of cost of benefits. Illustration 19-4 p. 1173 dbo continuity schedule. Interest accrues on dbo: based on dbo outstanding, aspe/ifrs both use market rate (current yield on high-quality debt, aspe allows settlement rate rate implied in insurance contract to effectively settle pension obligation. In estimating dbo actuaries make assumptions about variables mortality/turnover/retirement rate/ interest/inflation/salary: experience adjustment experience vary from assumption, revised assumptions gain/loss result. Illustrate: calculated dbo based on opeining balance of service/interest cost / benefits paid 962,000, actuaries adjustment to 975,000$ loss of 13,000$ Increase by return on plan asset difference between actual return & expected return using same rate as dbo: changes in plan assets.