ADMS 3595 Chapter Notes - Chapter 21: Book Value, Accounts Payable, Accrual

10 Mar 2018

School

Department

Course

Professor

Document Summary

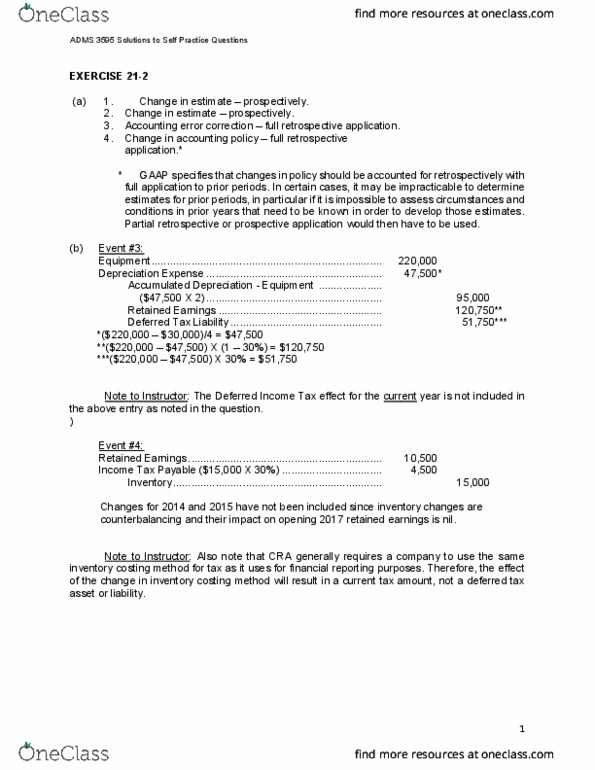

Adms 3595 ch 21 accounting changes & error analysis ra (retrospective application) Change in estimate of service life / change in estimate of nrv: correction of prior period error, prior period error omission / mistakes in fs of prior periods caused by misuse of information, ex. Failure to recognize depreciation: changes in accounting policies, choices of accounting policies. Initial choice of accounting policy based on gaap: aspe gaap hierarchy guidance to flow when no primary source of. Ifrs similar hierarchy: primary sources look to ifrs integral part of specific standard. Ifrs -one of following 2 situation required for change in accounting policy. Capitalize interest but no previous self construction activities: what if previous method unacceptable/applied incorrectly, not considered change considered correction of errors. If change in classification of items on fs change in presentation only & Interest reported as investing outflow (change from operating outflow) If full ra impracticable info why so / periods affected / how change handled.