ECON 2000 Chapter Notes - Chapter 17: Real Interest Rate, Fixed Investment, Marginal Product

18 Mar 2014

School

Department

Course

Professor

Document Summary

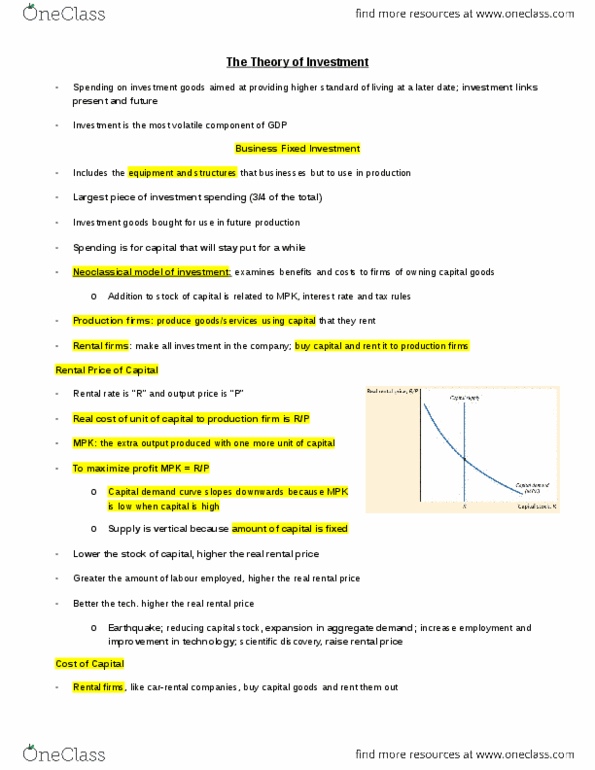

Business fixed investment includes the machinery, equipment, and structures that businesses buy to use in production. Residential investment includes the new housing that people buy to live in and that landlords buy to rent out. Inventory investment includes those goods that business put aside in storage, including materials and supplies, work in process, and finished goods. Includes everything from fax machines to factories, computers to company cars. The standard model of business fixed investment is called the neoclassical model of investment. This model examines the benefits and costs to firms of owning capital goods. To develop the model, imagine that there are two kinds of firms in the economy. Production firms produce goods and services using capital that they rent. Rental firms make all the investments in the economy; they buy capital and rent it out to the production firms. This is not usually the case in the real world, however it simplifies our analysis.