BUS 215 Chapter Notes - Chapter 2: Direct Labor Cost, Sunk Costs, Management Accounting

Document Summary

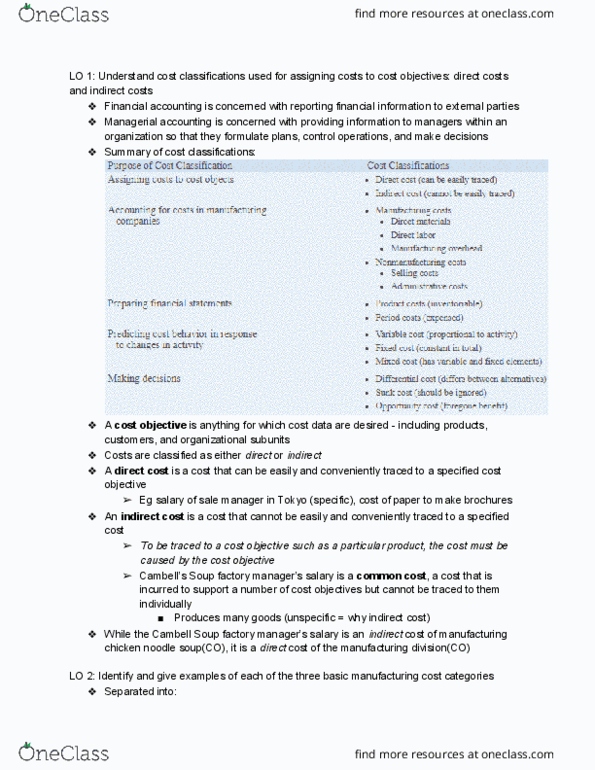

A cost object is anything for which cost data are desired including products, customers, jobs, and organizational subunits: costs are classified as either direct or indirect. Direct cost: a direct cost is a cost that can be easily and conveniently traced to a specified cost object. Cost classifications: direct cost (can be easily traced, indirect cost (cannot be easily traced) Predicting cost behavior in response to changes in activity. Behavior of the cost (within the relevant range) Variable cost total variable cost increases and decreases in. Variable cost per unit remains constant. proportion to changes in the activity level. Total fixed cost is not affected by changes in the activity level within the relevant range. Fixed cost per unit decreases as the activity level rises and increases as the activity level falls. Mixed costs: a mixed cost contains both variable and fixed cost elements.