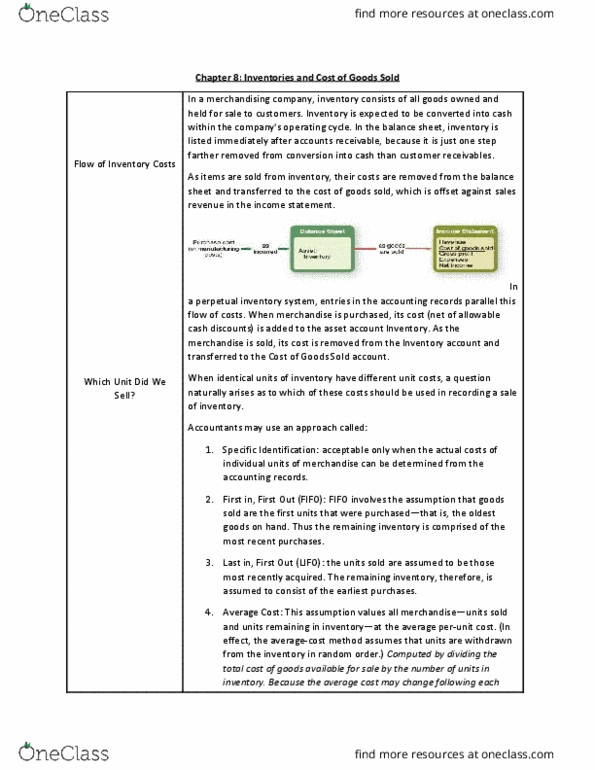

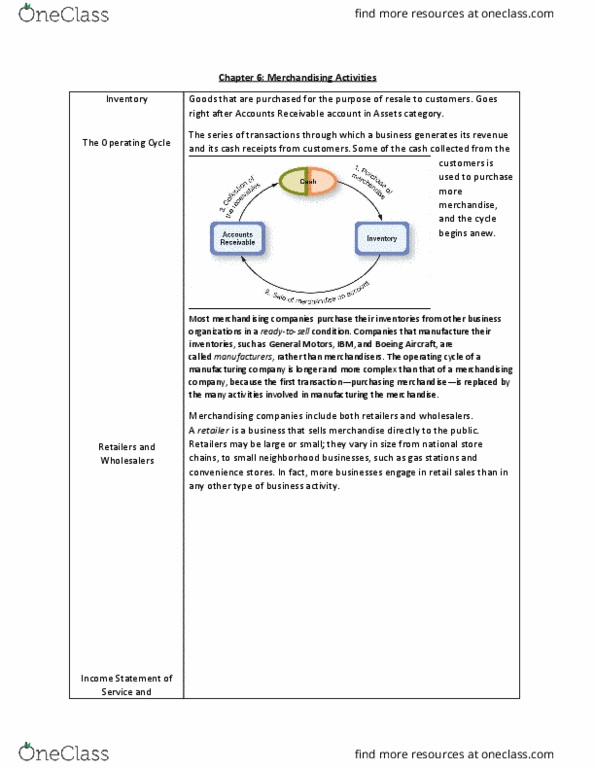

ACCT 115 Chapter 6: Accounting Chapter Six

Document Summary

Get access

Related Documents

Related Questions

Capes Corporation is a wholesaler of industrial goods. Data regarding the store's operations follow:

Sales are budgeted at $260,000 for November, $270,000 for December, and $250,000 for January.

Collections are expected to be 60% in the month of sale and 40% in the month following the sale.

The cost of goods sold is 60% of sales.

The company desires an ending merchandise inventory equal to 40% of the cost of goods sold in the following month. Payment for merchandise is made in the month following the purchase.

The November beginning balance in the accounts receivable account is $61,000.

The November beginning balance in the accounts payable account is $248,000.

Required:

a. Prepare a Schedule of Expected Cash Collections for November and December.

b. Prepare a Merchandise Purchases Budget for November and December.

Prepare a Schedule of Expected Cash Collections for November and December.

|

Prepare a Merchandise Purchases Budget for November and December.

|

Altira Corporation uses a periodic inventory system. Thefollowing information related to its merchandise inventory duringthe month of August 2018 is available:

| Aug.1 | Inventory on handâ2,000 units;cost $6.10 each. |

| 8 | Purchased 10,000 units for $5.50each. |

| 14 | Sold 8,000 units for $12.00each. |

| 18 | Purchased 6,000 units for $5.00each. |

| 25 | Sold 7,000 units for $11.00each. |

| 31 | Inventory on handâ3,000 units |

Determine the inventory balance Altira would report in itsAugust 31, 2018, balance sheet and the cost of goods sold it wouldreport in its August 2018 income statement using each of thefollowing cost flow methods.

FIFO

LIFO

Average Cost

Determine the inventory balance Altira would report in itsAugust 31, 2018, balance sheet and the cost of goods sold it wouldreport in its August 2018 income statement using the FIFO method.(Round "Cost per Unit" to 2 decimal places.)

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Determine the inventory balance Altira would report in itsAugust 31, 2018, balance sheet and the cost of goods sold it wouldreport in its August 2018 income statement using LIFO method.(Round "Cost per Unit" to 2 decimal places.)

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Determine the inventory balance Altira would report in itsAugust 31, 2018, balance sheet and the cost of goods sold it wouldreport in its August 2018 income statement using Average costmethod. (Round "Average Cost per Unit" to 2 decimal places.)

| ||||||||||||||||||||||||||||||||||||||||||||||||||||