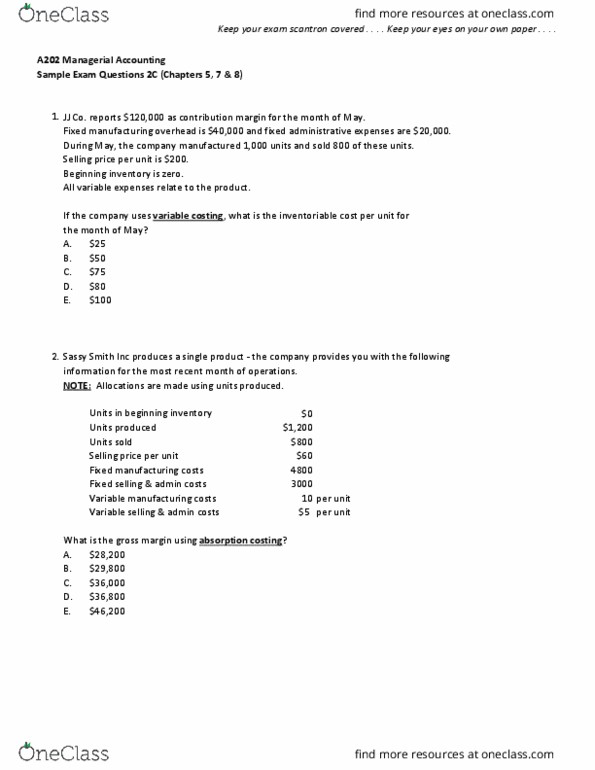

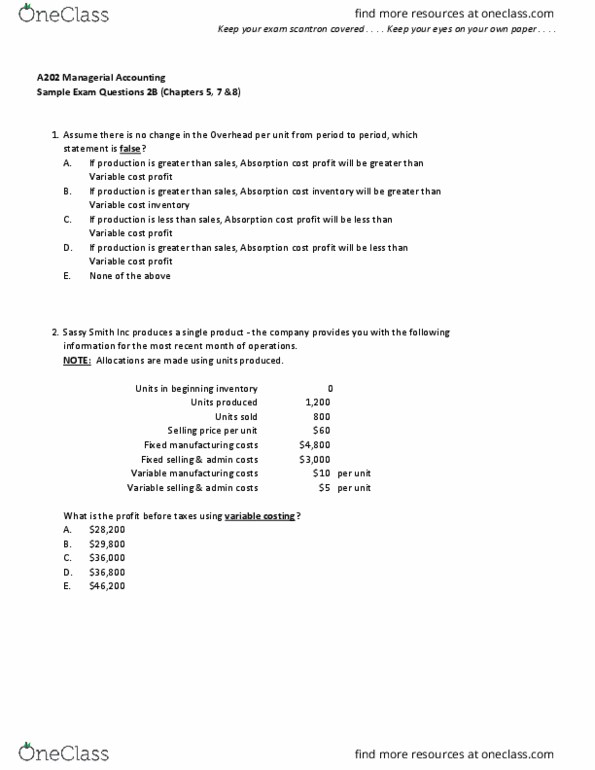

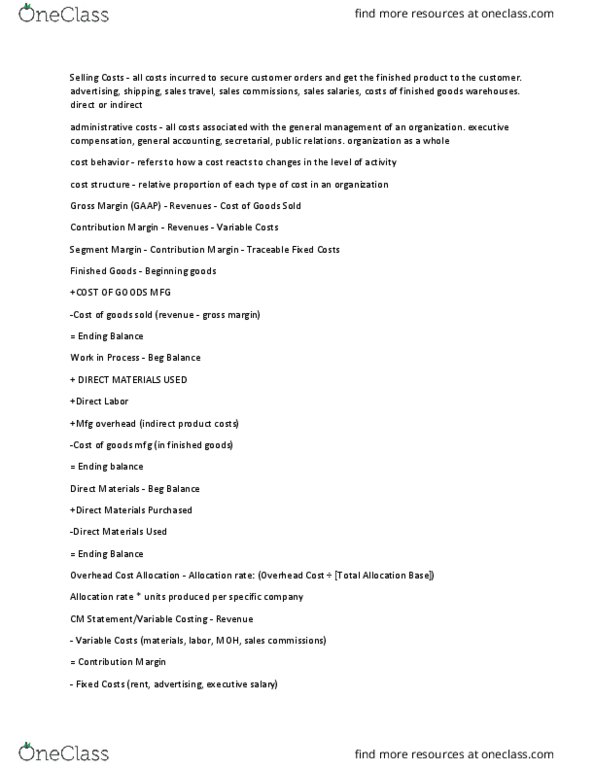

BUS-A 202 Chapter Notes - Chapter 5: Total Absorption Costing, Expense, Income Statement

Document Summary

Chapter 5: variable costing and segment reporting: tools for management. How manufacturing companies can prepare variable costing income statements, which rely on the contribution format, for internal decision making purposes. Segment- a part or activity of an organization about which managers would like cost, revenue, or profit data. Both income statement formats include product and period costs. Variable costing income statements are grounded in the contribution format. Absorption costing income statements ignore variable and fixed cost distinctions: variable costing. Only those manufacturing costs that vary with output are treated as product costs. Direct materials, direct labor, and the variable portion of manufacturing overhead. Fixed manufacturing overhead is treated as a period cost and it is expensed in its entirety each period: absorption costing. Treats all manufacturing costs as product costs, regardless of whether they are variable or fixed. Direct materials, direct labor, and both variable and fixed manufacturing overhead. Full cost method: selling and administrative expenses.