COB 241 Chapter Notes - Chapter 9: Contingent Liability, Going Concern, Financial Statement

1 Nov 2016

School

Department

Course

Professor

Document Summary

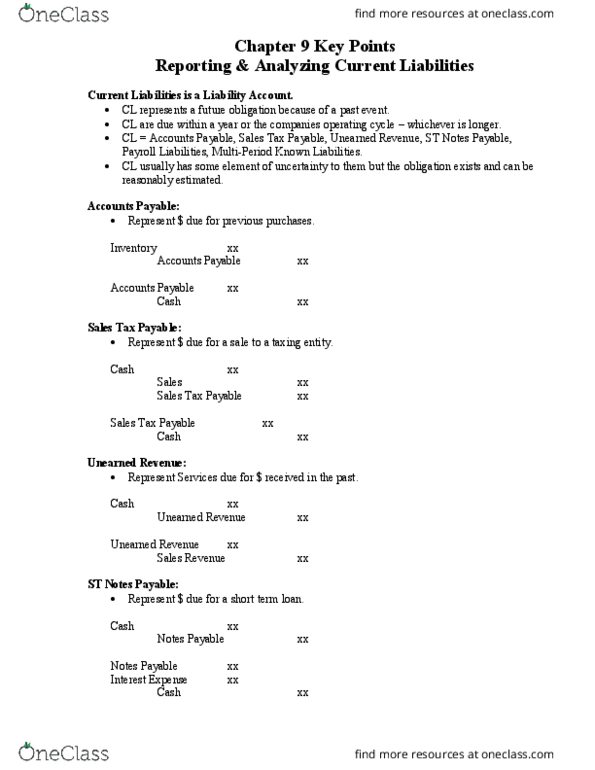

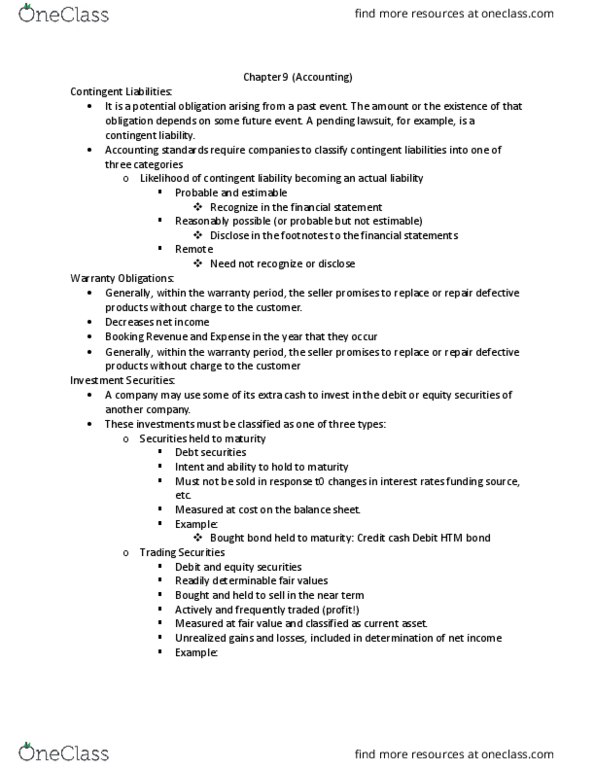

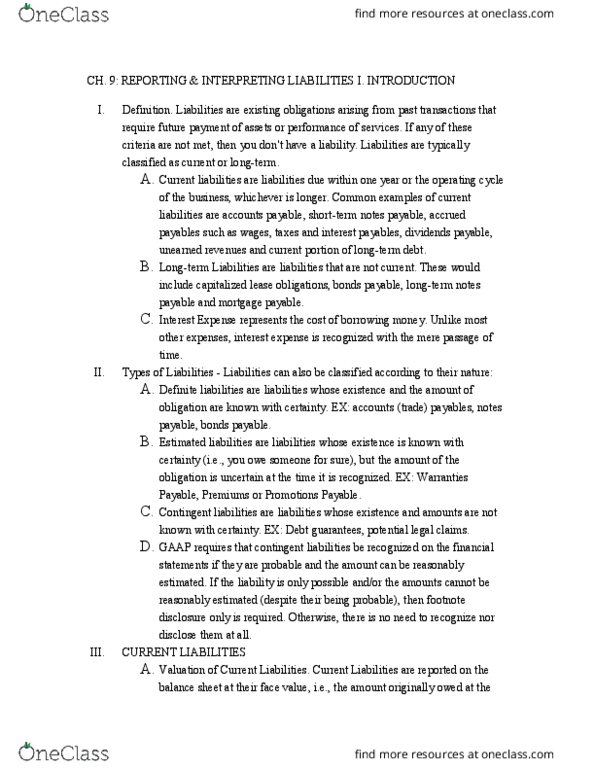

Unless there is evidence to the contrary, companies are assumed to be going concerns that will continue to operate. Under this assumption, companies expect to pay their obligations in full. Issuer: the maker of the note, who issues the note to the payee. Contingent liability: a potential obligation arising from a past event. Companies must classify contingent liabilities into three different categories: if the likelihood of a future obligation arising is probable (likely) and its amount can be reasonably estimated, a liability is recognized in the financial statements. The potential liability is, however, disclosed in the notes to the financial statements. Likelihood of a contingent liability becoming an actual liability. Disclose in the notes to the financial statements. Employee: the individual whose work is supervised by the business, directed, and controlled. Independent contractor: when a business pays an individual for specific services, but the individual supervises and controls the work.