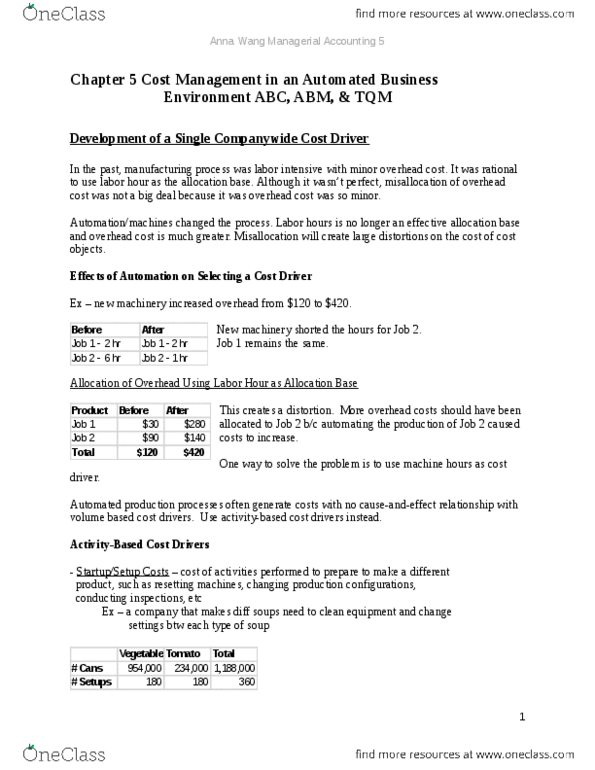

TAHOS CORPORATION

TAHOS CORPORATION buys coffee beans from around the world and roasts, blends, and packages them for resale. The major cost is direct materials; however, there is substantial manufacturing overhead in the predominately automated roasting and packaging process. The company uses relatively little direct labor.

Some of the coffees are very popular and sell in large volumes, whereas a few of the newer blends sell in very low volumes. TAHOS prices its coffee at budgeted cost, including allocated overhead, plus a markup on cost of 20%. A competitor charges $6.00 per pound of Alpha and $7.00 per pound for Beta.

Data for the 2017 budget include manufacturing overhead of $3,000,000, which has been allocated on the basis of each productâs budgeted direct labor cost. The budgeted direct labor cost for 2017 totals $600,000. Purchases and use of materials (mostly coffee beans) are budgeted to total $6,000,000.

The budgeted direct costs for one-pound bags of two of the companyâs products are:

ALPHA BETA

Direct materials $4.20 $3.20

Direct labor .30 .30

TAHOS believes the existing traditional costing system may be providing misleading information. He has developed an activity based analysis of the 2017 budgeted manufacturing overhead costs, which is shown in the following table:

Activity Cost Driver Cost-Driver Rate

Purchasing Purchase Orders $500

Materials handling Number of parts 400

Quality control Batches 240

Roasting Roasting hours 10

Blending Blending hours 10

Packaging Packaging hours 10

Budgeting data for the 2017 production of the two products follow. There will be no beginning or ending inventories for either of these coffees.

ALPHA BETA

Expected sales 100,000 pounds 2,000 pounds

Purchase orders 4 4

Batches 10 4

Number of parts 30 12

Roasting hours 1,000 20

Blending hours 500 10

Packaging hours 100 2

Required:

1. Calculate the 2017 budgeted manufacturing overhead rate using direct labor cost as the single cost driver.

2. Calculate the 2017 budgeted cost for one pound of each ALPHA and BETA and the corresponding selling price using direct labor cost as the single cost driver.

3. What decisions would you suggest be made given the competitorâs prices for the two products?

________________________________________________________________

4. Using ABC, recalculate the 2017 budgeted cost for one pound of each ALPHA and Beta and the corresponding selling price.

5. Explain how company decisions would be different using ABC rather than the traditional costing system.

6. Explain how activity-based management (ABM) is useful to (1) reduce cost, (2) speed up the manufacture, and (3) improve the quality of the two coffees.