ACCT 2301 Chapter Notes - Chapter 5: Activity-Based Costing, Cost Driver, Total Quality Management

2 Mar 2016

School

Department

Course

Professor

Document Summary

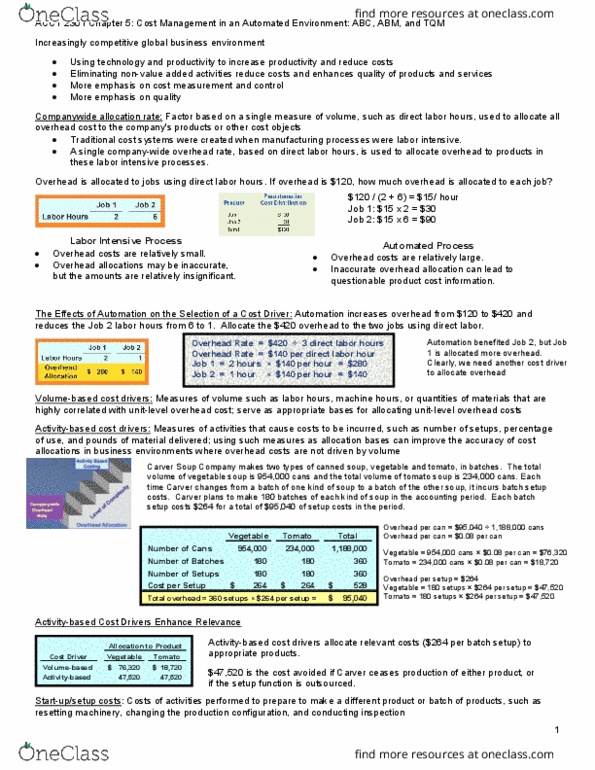

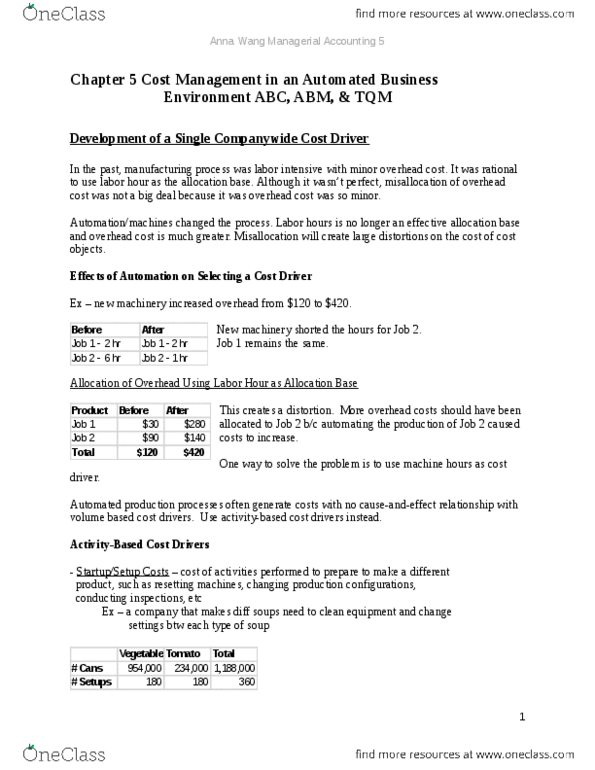

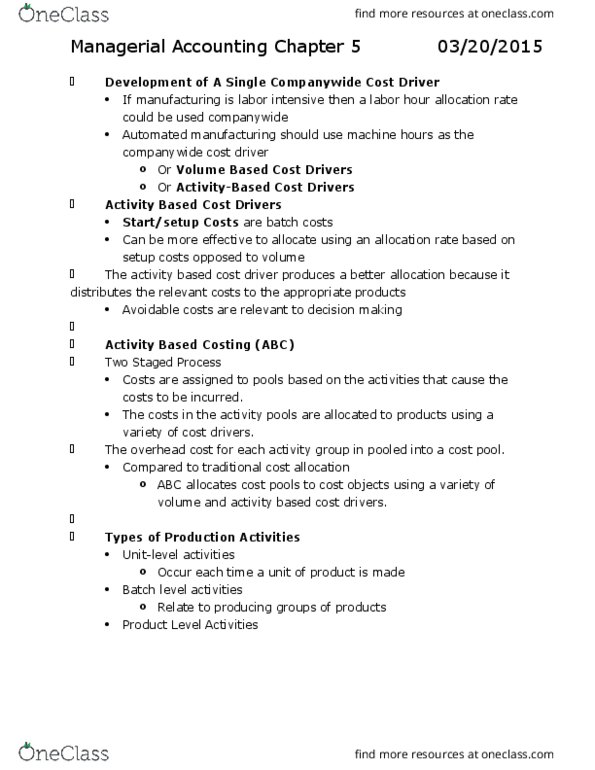

Chapter 5: cost management in an automated business environment: abc, abm, and. Many companies use direct labor hours as the sole base for establishing a companywide allocation rate. Automation changed the nature of the manufacturing process so direct labor hours is no longer effective in many modern companies: machines replacing workers generating most production, remaining workers are highly skilled. Greater automation has greater overhead costs (utility, and depreciation charges) Automation requires a change in cost driver to machine hours: companies have adopted activity based cost drivers to improve the accuracy of indirect cost allocations. Start-up or setup costs: costs are incurred for each new batch. When using volume based allocation rate, it overcosts high volume product and undercosts the low volume product. Activity based costs driver (number of setups) provides a more accurate allocation base for setup costs. Activity based cost driver produces a better allocation b/c it distributes the relevant costs to appropriate products.