ACCT 421 Chapter Notes - Chapter 6: Alimony, Passive Income

3 Oct 2016

School

Department

Course

Professor

Document Summary

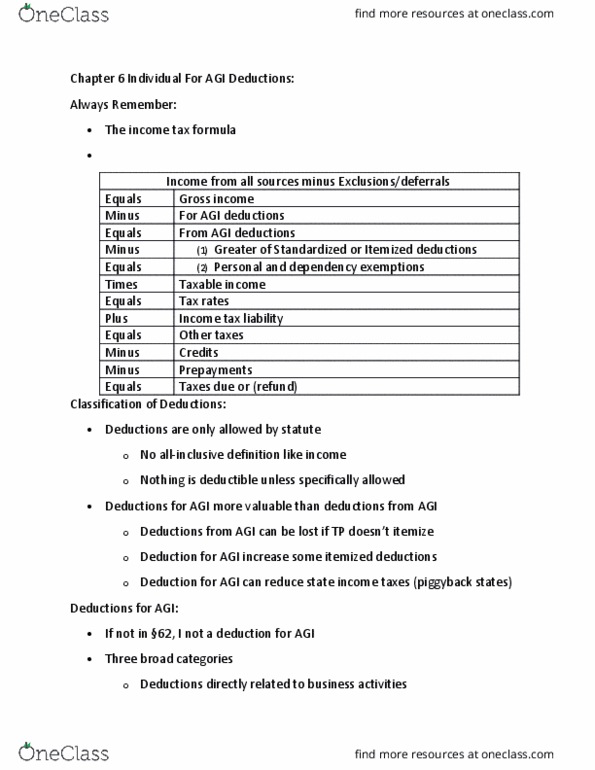

Lo 6-1: identify for agi deductions directly related to business activities. The deductions for agi directly related to business activities include business expenses, rent and royalty expenses, losses from the disposition of business assets, and expenses and losses incurred by flow-through entities. Business deductions are reported with business revenues on schedule c. Rent and royalty expenses and losses incurred by flow-through entities, which pass through to their owners, are reported on schedule e. Lo 6-2: describe the loss limitation rules for passive activities, rental use of a home, and home office deductions. A taxpayer"s share of operating losses from flow-through entities and other trade or business activities are deductible to the extent they clear the tax- basis, at-risk, and passive activity loss hurdles. A taxpayer"s passive losses from an activity are limited to passive income from all other sources until disposition of the activity. On disposition, current and prior passive losses from an activity can be used without limitation.