ACC-1A Chapter Notes - Chapter 8: Sunk Costs, Outsourcing

Document Summary

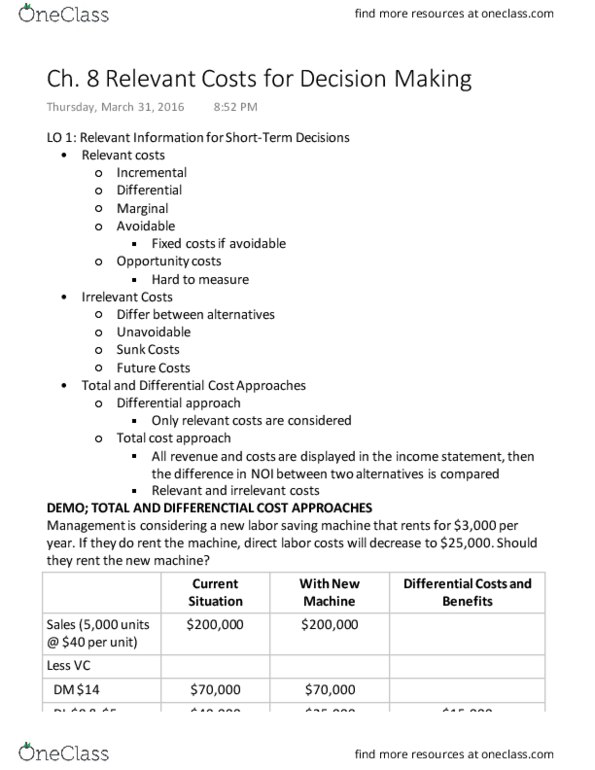

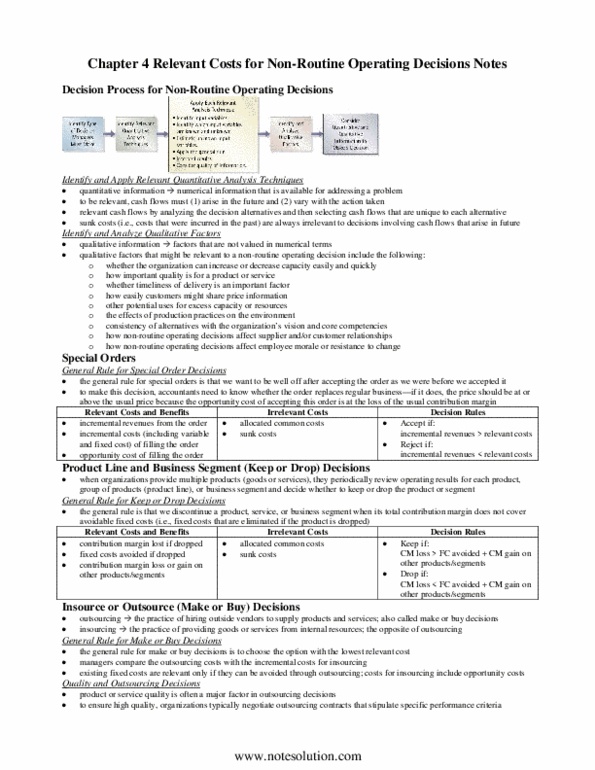

Costs that change as a result of decision. Variable expenses, fixed costs (direct fixed costs change, allocated costs do not change), avoidable costs change (unavoidable do not!) Costs that do not change are not relevant. Sunk costs, allocated cost, unavoidable costs, common costs. Understand business context associated with each of four short term decisions. Each st decision has costs and benefits. Shifted units= available units - special order units. Ve= dm, dl, moh, direct fixed expenses, commission. = number of units outsource * outsource price. Benefits= cost that go away when you outsource. Benefits could also include additional revenue from outsourcing; such as if we outsource, more space that we can lease for money. Get rid of all ve associated with line: sales revenue, ve, Keep costs that do not go away (not relevant costs) Keep the line if new operating income < old one. If there is a resource constraint - need to figure out production order.