BMGT 220 Chapter Notes - Chapter 2: Retained Earnings, Accounting Equation, Income Statement

14 Sep 2016

School

Department

Course

Professor

Document Summary

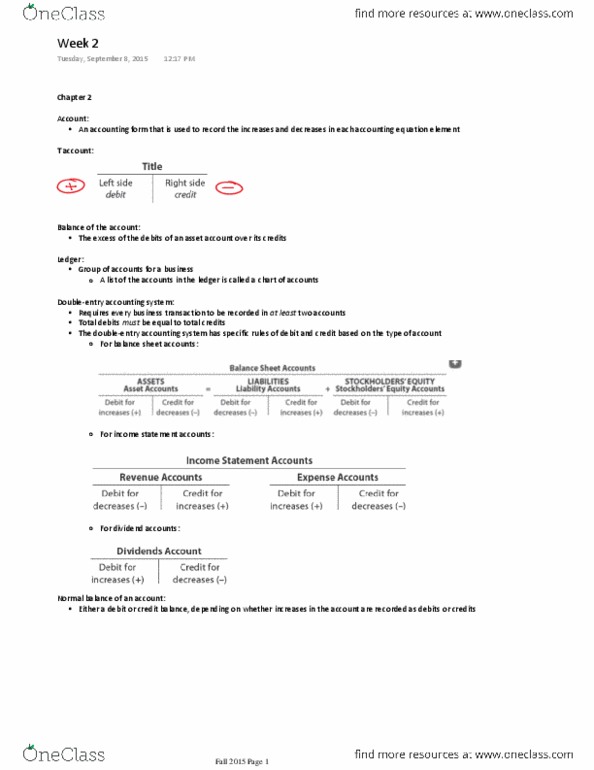

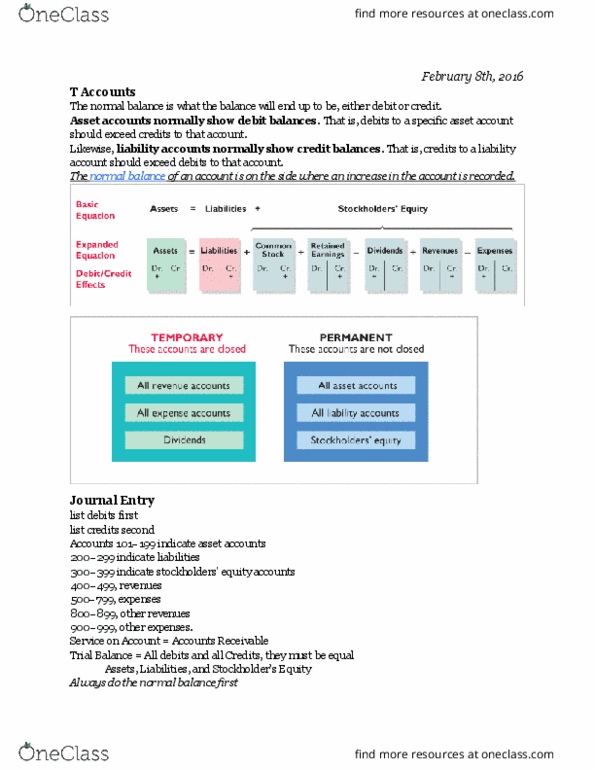

Accounting systems are designed to show the increases and decreases in each accounting equation element as a separate record, called an account. A title: name of the accounting equation element recorded in the account. A space for recording increases in the amount of the element. A space for recording decreases in the amount of the element. The resulting representation (of account described above) is a t account, in which the left side of the account is called the debit side, and the right side is called the credit side. For assets, increases in the account are recorded on the debit (left side of the account) and decreases on the credit (right side) of an account. The excess of the debits of an asset account over its credits is the balance of the account. Assets - resources owned by a business entity, i. e. cash, supplies, intangibles (copyrights) Liabilities - debts owned to outsiders (creditors), i. e. accounts payable, unearned revenue.