BMGT 350 Chapter Notes - Chapter 9: Price Ceiling, Price Floor, Target Costing

22 Apr 2016

School

Department

Course

Professor

Document Summary

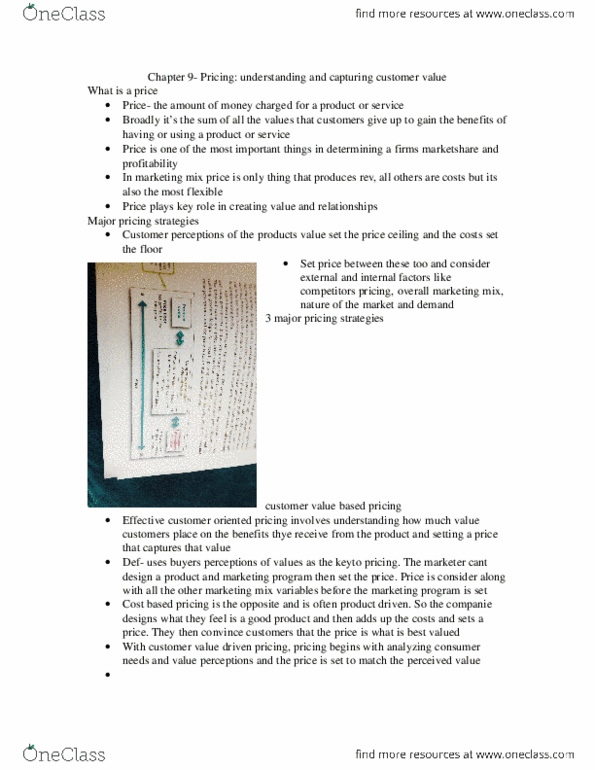

Chapter 9- pricing, understanding and capturing customer value. Product cost set floor for a product"s price: company prices product below its costs, company"s profits will suffer. Three major pricing strategies: customer value-based pricing, cost-based pricing, competition-based pricing. Customer value-based pricing pricing decision must start with customer value. Considerations in setting price: product costs: No profits below this price: competition and other external factors: No demand above the price cost-based pricing: design a good product, determine product costs. Aldi practices an important type of good-value pricing at the retail level called everyday low pricing (edlp) Edlp involves charging a constant, everyday low price with few or no temporary price discounts. Retailers such as costco practice edlp but wal-mart is the king. High-low pricing-chagrining higher prices on an everyday basis but running frequent promotions to lower prices temporarily on selected items: kohl"s and macy"s have frequent sale days early-bird savings, bonus earnings for store credit-card holders.