ECON 200 Chapter Notes - Chapter 14: Average Variable Cost, Market Power, Marginal Revenue

11 Mar 2014

School

Department

Course

Professor

Document Summary

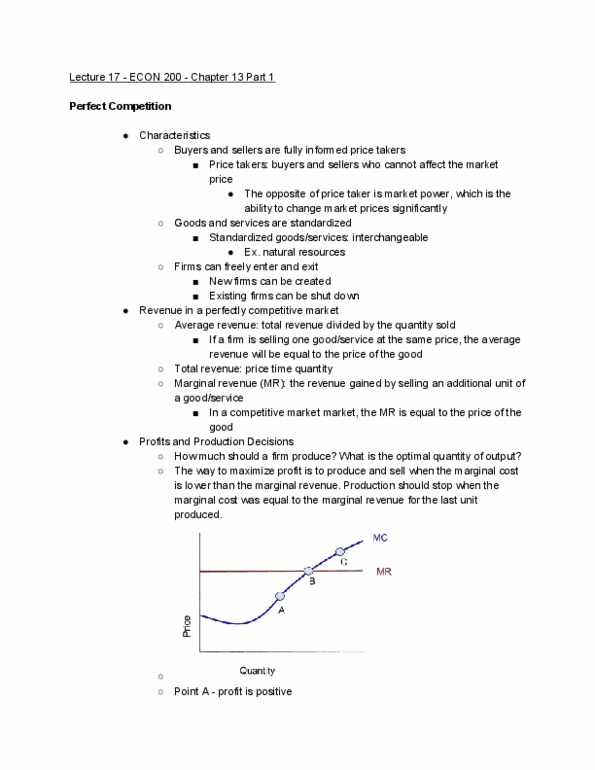

Competitive market: many buyers and sellers trading identical products so that each buyer and seller is a price taker. Price takers: buyers and sellers must accept the price the market determines. Cant influence market price because production is such small part of total. Firms can freely enter and exit the market. Small firms: can"t change market price, but can increase quantity to increase. Average revenue: total revenue (pxq) divided by the quantity sold (x). All firms" average revenue equals the price of the good. Marginal revenue: the change in total revenue from an addition unit sold. Marginal revenue equals the price of the good (average revenue) (competitive revenue. markets) If marginal revenue is greater than marginal cost you should increase production, and vice versa. The marginal cost curve determines the quantity of the good the firm is supplying, so it is the supply curve. Shut down: short run decision to not produce anything for a specific time period.