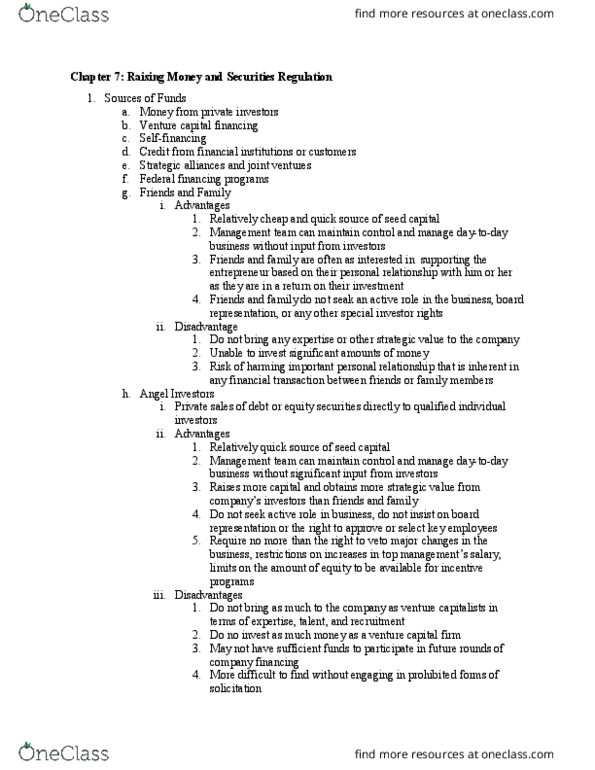

BSL 435 Chapter Notes - Chapter 13: Initial Public Offering, Preferred Stock, Cash Flow

1 May 2018

School

Department

Course

Professor

Chapter 13: Venture Capital

1. Deciding whether to seek venture capital

a. Determine whether the new business will meet the criteria used by most VCs

i. A potential to grow to a significant size quickly and to generate an annual

return on investment in excess of 40% over a period of 3 to 5 years.

b. VCS mainly focus on technology industry and life science companies

c. Attractive source of funding because

i. Allow entrepreneur to raise all capital from one source or from lead

investor that can attract other investors

ii. VCs understand the challenges of start-ups and have experience growing a

company to an initial public offering, a sale of the business, or other

liquidrt event

iii. VCs have network of contacts

iv. Can provide assistance in recruiting other members of the management

team and in eastablishing high-level contacts among potential key

customers

v. Excellent board members

vi. Venture-backed firm tend to raise more money, gorw more quickly, secure

more patents, and have higher market share

vii. Firms also perform significantly better when they go public

d. VCs look for companies that can provide liquidity in three to five years, so if an

entrepreneur is looking for a longer time horizon, the enterprise may not be

suitable for venture capital.

e. Avoid venture capitals

i. VCs are more sophisticated negotiators and may drive a hardere bargain

on the pricing and terms of their investment than friends and family

ii. VCs may be more likely to art their power in molding the enterprise than

more passive investors

iii. VCs may be more interested than passive investors in replacing the

management team or taking control of the enterprise if the entrepreneur

stumbles

iv. Family, friends, and angels may be willing to pay a higher price and tend

to require less onerous investment terms and conditions than VCs, but they

often bring little else to the table and are unlikely to make substantial

follow-on investments

2. Finding venture capital

a. Arrange an introduction by someone who knows the venture capitalist

b. Engage a lawyer who works primarily in the venture capital field as a business

attorney

3. Selecting a venture capitalist

a. Business plans

i. Should be more concise and less legalistic than information statements or

offering documents prepared for other investors

ii. Describes product or service concept and opportunity for investors

find more resources at oneclass.com

find more resources at oneclass.com

iii. Includes sections describing industry, market, means for producing the

product or delivering the service, competition, superiority of product or

service, marketing plan, IP, strength of management team

iv. Projection

v. Summary on top

vi. Pitfalls

1. Too long: more than 15 or 20 pages

2. Summary is too long

a. Should be one page

b. Describe the market, unment need in the market,

compelling solution offered by entrepreneur, strategy for

connecting the need, solution, and customers, the

techmology or other proprietary aspects of solution that

will give this venture an edge over the competiion

c. Experience of team that demonstrates that the plans can be

implemented

d. How much money is being raised and what the company

plans to accomplish with the funding

3. Opportunity is too small

4. Plan is poorly organized

5. Plan lacks focus

b. Courtship Process

i. Tqkes two or three months

ii. VCS perform due diligenc,e the process through which VC examines

company concept, product, potential market, financial nealth, and legal

situation

iii. Entrepreneur performs due diligence

c. Multiple Investors

i. It might be advantageous to attract and accommodate more than one VC

in a round

1. Increase network of resources available to company

2. Can serve as a counterbalance if the entrepreneur and first VC end

up at loggerheads on an issue

ii. In raising money during a subsequent round of VC, you should tell the

new investor that the prior-round VC investor wants to maintain or

increase their stake

iii. New VC can take the lead in negotiating with the company the price and

other terms of the stock to be sold in the subsequent round

iv. Once the price is set, the lead investors from the prior round will indicate

how much stock they will buy

4. Determining the Valuation

a. Pricing terminology

i. Pre-money and post-money refer to the valuation that is put on the

company before and after the investment

1. If a VC will invest $2 million, and they say they will put in the $2

million based on three pre-money, this means that the VC is

find more resources at oneclass.com

find more resources at oneclass.com

proposing that the company is worth $3 million before their

investment and is now worth $5 million after the investment

ii. “I’m thinking two-thirds based on three pre-; that will get you to five post-

“

1. This means that the VC is requesting ownership share equivalent to

66% of equity based on pre-money number and 40% post-money

b. Negotiating Price

i. A VC may ask what valuation the company is seeking or may volunteer a

ballpark figure for pricing

ii. VC will base valuations on magement’s own projections and on deals

done in the industry by other companies

c. Effects of Shares in Option Pool

i. Entrepreneur should understand how reservation of shares for future stock

issuances too employees will affect the price per share

1. If VC offer of $2 million is for 40% of the company including the

reservation of 1 million shares for options, then he or she is saying

that there are 7 million shares outstanding or reserved, so 7 million

is what needs be taken into account when calculating the 40%

ii. If this is not what you had in mind, the company should propose that the 1

million reserved shares not be taken into account in the valuation

d. Choosing among firms

i. VC willing to pay the highest price is not necessarily the firm that you

should most want in the deal

ii. Another VC may be a better partner in growing the business or in

attracting investors for future rounds

iii. Undertake due diligence in the form of reference checks

iv. What’s most important is maximizing the valuation of their stake on exit,

and not necessarily the valuation in any particular round

5. Rights of Preferred Stock

a. Preference on liquidation

b. Pays higher dividend than common stock

c. Convertible at any time at the election of the holder and automatically converts

upon the occurrence of certain events

d. Votes on an as-if-converted-to-common basis and may have special voting rights

with respect to the election of directors and certain other events

e. Mandated redemption provision, requiring the company to buy back the stock at a

set price on a given date in the future if the investor requests

f. Downside and Sideways Protection

i. When negotiating the rights and privileges afforded the holders of

preferred stock, entrepreneurs should keep in mind that if all goes well and

the venture performs as projected, the VCs will convert their preferred

stock into common stock

ii. Upon conversion, the protective devices will have had little or no effect on

the return to the founders and the other holders of common stock

iii. If the company declines in value or moves sideways, then the VCs will not

convert their preferred stock and will rely on their rights and preferences

find more resources at oneclass.com

find more resources at oneclass.com