MGMT 30A Chapter Notes -Legal Personality, Accounts Payable, Sole Proprietorship

11 Oct 2013

School

Department

Course

Professor

7

MGMT 30A Full Course Notes

Verified Note

7 documents

Document Summary

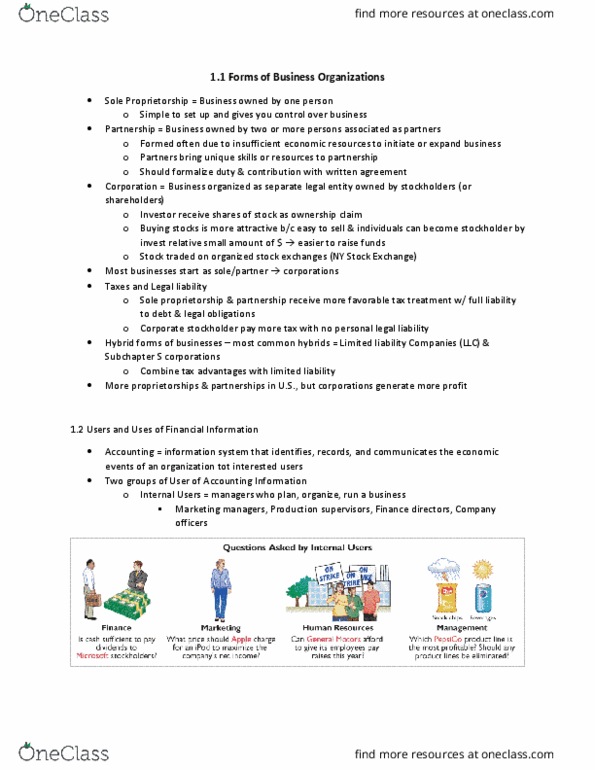

Mgmt30a ch1: forms of business organizations sole proprietorship: business owned by 1 person, simple to set up, gives you control, tax advantages. Partnership: business owned by 2 or more people associated as individual doesn"t have enough eco. Creditors: suppliers, bankers evaluate risks of selling on credit/lend $ taxing authorities: (irs) see if comp comply to tax laws. Labor unions see if owners will have ability to increase wage/benefits. Business activities financing: personal savings/cash from banks investing: cash into equipment to run business: operating: making & sell, accounting information system: keeps track of results of each business activities (finance, invest, operating, financing activities sources of outside funds. Borrow 22597 or sell stock loan or borrow from investors (bonds) liabilities: amount owned to creditors: note payable: bank for the money borrowed, bonds payable: debt sold to investors must be repaid by particular date.