MGMT 30A Chapter Notes - Chapter 4: Income Statement, Deferral, Accrual

7

MGMT 30A Full Course Notes

Verified Note

7 documents

Document Summary

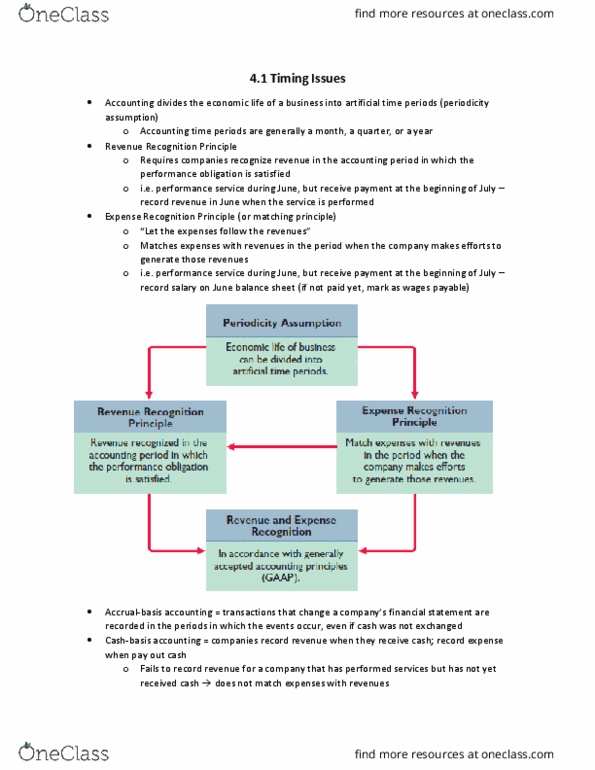

Timing issues accountants divide the economic life of a business into artificial time periods (periodicity assumption) o ex. a month, a quarter, or a year calendar year (january-december) vs. fiscal year (ex. October 1-september 30) o companies try to match the fiscal year of their competitors (this creates transparency; makes it easier to compare the company with its competitors) Review question (quiz) periodicity assumption: the economic life of a business can be divided into artificial time periods. The revenue recognition principle companies recognize revenue in the accounting period in which the performance obligation (performing obligation based on the contract made) is satisfied. Match expenses (costs) with revenues in the period when the company makes efforts to generate those revenues. Accrual transactions recorded in the periods in which the events occur revenues recognized when services performed, even if cash wasn"t received expenses recognized when incurred, even if cash wasn"t paid. Cash-basis records things based on cash received and cash paid.