MGT 5 Chapter Notes - Chapter 10: Budget, Variable Cost

31 Jul 2017

School

Department

Course

Professor

Document Summary

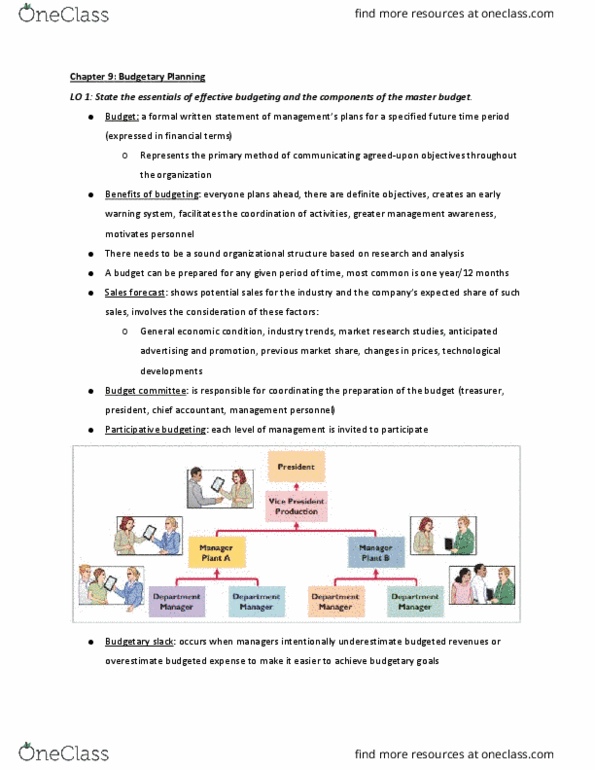

Lo 1: describe budgetary control and static budget reports. Budget reports: compares actual results with planned objectives, helps firms control budgets. Identifies the name of the budget report, such as the sales budget or the manufacturing overhead budget. States the frequency of the report, such as weekly or monthly. Static budget: projection of budget data at one level of activity. Uses and limitations: the actual level of activity closely approximates the master budget activity level, and/or the behavior of the costs in response to changes in activity is fixed. Flexible budget: projects budget data for various levels of activity; the flexible budget is a series of static budgets at different levels of activity. Identify the activity index and the relevant range of activity. Identify the variable costs, and determine the budgeted variable cost per unit of activity for each cost. Identify the fixed costs, and determine the budgeted amount for each cost.