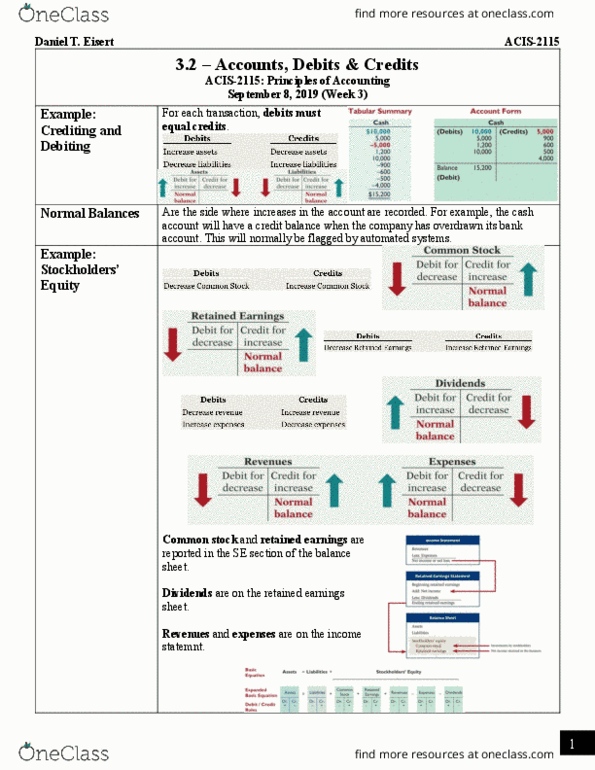

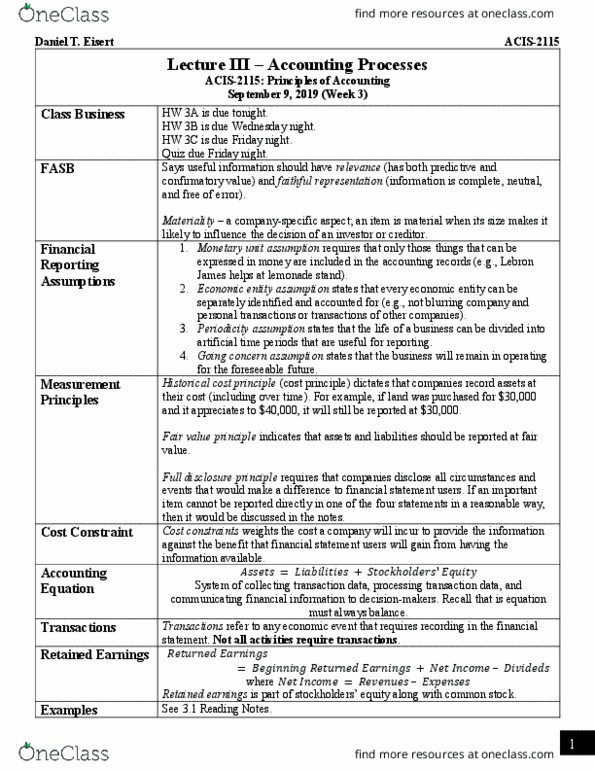

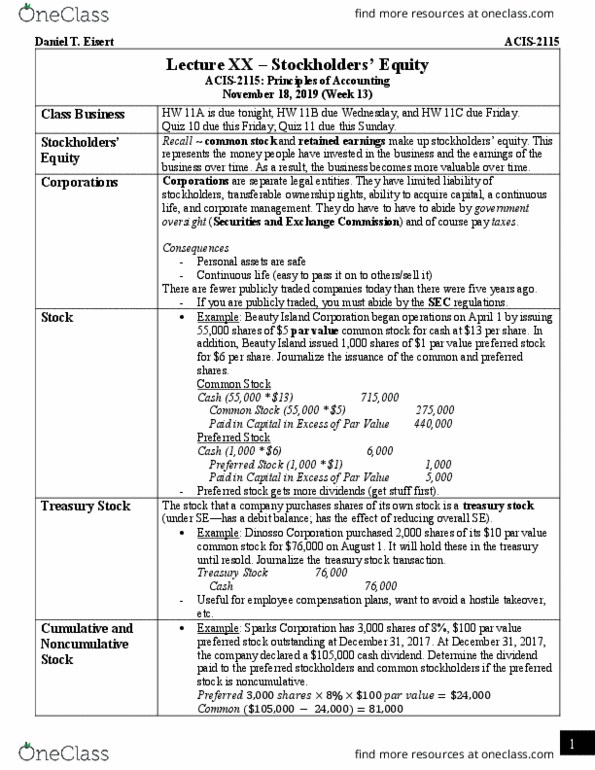

ACIS 2115 Chapter 3.3: ACIS 2115 Chapter 3.: ACIS-2115 - Reading Notes - 3-3- Journals

Get access

Related Documents

Related Questions

PLEASE FOLLOW THE INSTRUCTIONSâ

Assignment: Special Journals: Sales and Cash Receipts (12 Points)

Prepare a cash receipts journal based on the information given below and post it to the Accounts Receivable Subsidiary Ledger.

On Nov 17, Ms. Don & Co. received $1,450 from Gians Graze to apply on account. The source document for this transaction is Receipt 30.

Instructions:

1. Prepare a sales journal entry based on the information given above and post it to the Accounts Receivable General Ledger account and to the Accounts Receivable Subsidiary Ledger. (Use November 7 for this transaction date.) ***This is the same entry that you made for the previous assignment. However, use the transaction date given (Nov. 7).

2. Enter the above transaction (Nov 17) into the Cash Receipts Journal and post it to the Accounts Receivable General Ledger account and to the Accounts Receivable Subsidiary Ledger.

3. Prepare a Schedule of Accounts Receivable and check to see that the total agrees with the Accounts Receivable ledger account.

| Sales Journal | ||||||

| Date | Doc. No. | Customer's Account Name | Post Ref. | Sales Credit | Sales Tax Payable Credit | Accounts Receivable Debit |

| Cash Receipt Journal | ||||||||

| Date | Doc. No. | Account Name | Post Ref. | Sales Credit | Sales Tax Payable Credit | Account Receivable Credit | Sales Discount Credit | Cash in Bank Debit |

| Date | Particulars | Post ref. | Debit | Credit | Balance | |

| Debit | Credit | |||||

| Ms. Don & Co. Schedule of Accounts Receivable November 30, 20xx | ||

| Account Name | Amount | |

| Total Accounts Receivable | $ |

Purchases and Cash Payments Journals; Accounts Payable Subsidiary and General Ledgers

AquaFresh Water Testing Service was established on April 16. AquaFresh uses field equipment and field supplies (chemicals and other supplies) to analyze water for unsafe contaminants in streams, lakes, and ponds. Transactions related to purchases and cash payments during the remainder of April are as follows:

| April 16. | Issued Check No. 1 in payment of rent for the remainder of April, $3,500. | |

| April 16. | Purchased field supplies on account from Hydro Supply Co., $5,340. | |

| April 16. | Purchased field equipment on account from Pure Equipment Co., $21,450. | |

| April 17. | Purchased office supplies on account from Best Office Supply Co., $510. | |

| April 19. | Issued Check No. 2 in payment of field supplies, $3,340, and office supplies, $400. | |

| Post the journals to the accounts payable subsidiary ledger. | ||

| April 23. | Purchased office supplies on account from Best Office Supply Co., $660. | |

| April 23. | Issued Check No. 3 to purchase land, $140,000. | |

| April 24. | Issued Check No. 4 to Hydro Supply Co. in payment of April 16 invoice, $5,340. | |

| April 26. | Issued Check No. 5 to Pure Equipment Co. in payment of April 16 invoice, $21,450. | |

| Post the journals to the accounts payable subsidiary ledger. | ||

| April 30. | Acquired land in exchange for field equipment having a cost of $12,000. | |

| April 30. | Purchased field supplies on account from Hydro Supply Co., $7,650. | |

| April 30. | Issued Check No. 6 to Best Office Supply Co. in payment of April 17 invoice, $510. | |

| April 30. | Purchased the following from Pure Equipment Co. on account: field supplies, $1,340, and field equipment, $4,700. | |

| April 30. | Issued Check No. 7 in payment of salaries, $29,400. | |

| Post the journals to the accounts payable subsidiary ledger. |

Required:

1. Journalize the transactions (in chronological order as presented in the data) for April. Use a purchases journal and a cash payments journal, and a two-column general journal. Use debit columns for Field Supplies, Office Supplies, and Other Accounts in the purchases journal. Refer to the following partial chart of accounts:

| 11 | Cash | 19 | Land |

| 14 | Field Supplies | 21 | Accounts Payable |

| 15 | Office Supplies | 61 | Salary Expense |

| 17 | Field Equipment | 71 | Rent Expense |

At the points indicated in the narrative of transactions, post to the following accounts in chronological order in the accounts payable subsidiary ledger:

| Best Office Supply Co. |

| Hydro Supply Co. |

| Pure Equipment Co. |

For those boxes in which no entry is required, leave the box blank. If no other account is needed in the "Other Accounts Dr." column select "No Entry Required".

| PURCHASES JOURNAL | PAGE 1 | |||||||

|---|---|---|---|---|---|---|---|---|

| Date | Account Credited | Post. Ref. | Accounts Payable Cr. | Field Supplies Dr. | Office Supplies Dr. | Other Accounts Dr. | Post. Ref. | Amount |

| April 16 | Hydro Supply Co. | ? | No Entry Required | |||||

| April 16 | Pure Equipment Co. | ? | Field Equipment | |||||

| April 17 | Best Office Supply Co. | ? | No Entry Required | |||||

| April 23 | Best Office Supply Co. | ? | No Entry Required | |||||

| April 30 | Hydro Supply Co. | ? | No Entry Required | |||||

| April 30 | Pure Equipment Co. | ? | Field Equipment | |||||

| April 30 | ||||||||

| CASH PAYMENTS JOURNAL | PAGE 1 | |||||

|---|---|---|---|---|---|---|

| Date | Ck. No. | Account Debited | Post. Ref. | Other Accounts Dr. | Accounts Payable Dr. | Cash Cr. |

| April 16 | Rent Expense | |||||

| April 19 | Field Supplies | |||||

| Office Supplies | ||||||

| April 23 | Land | |||||

| April 24 | Hydro Supply Co. | ? | ||||

| April 26 | Pure Equipment Co. | ? | ||||

| April 30 | Best Office Supply Co. | ? | ||||

| April 30 | Salary Expense | |||||

| April 30 | Total | |||||

| JOURNAL | PAGE 1 | |||

|---|---|---|---|---|

| Date | Description | Post. Ref. | Debit | Credit |

| April 30 | Land | |||

| Field Equipment | ||||

2. Post the individual entries in chronological order (Other Accounts columns of the purchases journal and the cash payments journal and both columns of the general journal) to the appropriate general ledger accounts. Post to the subsidiary ledger in chronological order. When posting to the general ledger, post in chronological order. However, if there is more than one entry on the same date, post transactions from the purchases journal first, then the cash payments journal before posting from the general journal.

3. Total each of the columns of the purchases journal and the cash payments journal, and post the appropriate totals to the general ledger.

For those boxes in which no entry is required, leave the box blank.

| ACCOUNTS PAYABLE SUBSIDIARY LEDGER | |||||

|---|---|---|---|---|---|

| Date | Item | Post. Ref. | Debit | Credit | Balance |

| Account: Best Office Supply Co. | |||||

| April 17 | |||||

| April 23 | |||||

| April 30 | |||||

| Account: Hydro Supply Co. | |||||

| April 16 | |||||

| April 24 | |||||

| April 30 | |||||

| Account: Pure Equipment Co. | |||||

| April 16 | |||||

| April 26 | |||||

| April 30 | |||||

Post transactions in chronological order. However, if there is more that one transaction on the same date, post from the purchases journal first, then from the cash payments journal before posting from the general journal. (Because the problem does not include transactions related to cash receipts, the cash account in the ledger will have a credit balance.)

| GENERAL LEDGER | ||||||

|---|---|---|---|---|---|---|

| Balance | ||||||

| Date | Item | Post. Ref. | Debit | Credit | Dr. | Cr. |

| Account: Cash #11 | ||||||

| April 30 | ||||||

| Account: Field Supplies #14 | ||||||

| April 19 | ||||||

| April 30 | ||||||

| Account: Office Supplies #15 | ||||||

| April 19 | ||||||

| April 30 | ||||||

| Account: Field Equipment #17 | ||||||

| April 16 | ||||||

| April 30 | ||||||

| April 30 | ||||||

| Account: Land #19 | ||||||

| April 23 | ||||||

| April 30 | ||||||

| Account: Accounts Payable #21 | ||||||

| April 30 | ||||||

| April 30 | ||||||

| Account: Salary Expense #61 | ||||||

| April 30 | ||||||

| Account: Rent Expense #71 | ||||||

| April 16 | ||||||

4. Prepare a schedule of the accounts payable creditor balances.

| AQUAFRESH WATER TESTING SERVICE Accounts Payable Creditor Balances April 30 | |

|---|---|

| Best Office Supply Co. | $ |

| Hydro Supply Co. | |

| Pure Equipment Co. | |

| Total accounts payable | $ |

5. All are reasons why AquaFresh might consider using a subsidiary ledger for the field equipment EXCEPT:

To secure lower pricing on equipment purchases

American Laser, Inc., reported the following account balances on January 1. Accounts Receivable $ 5,000 Accumulated Depreciation 30,000 Additional Paid-in Capital 90,000 Allowance for Doubtful Accounts 2,000 Bonds Payable 0 Buildings 247,000 Cash 10,000 Common Stock, 10,000 shares of $1 par 10,000 Notes Payable (long-term) 10,000 Retained Earnings 120,000 Treasury Stock 0 The company entered into the following transactions during the year. Jan. 15 Issued 5,000 shares of $1 par common stock for $50,000 cash. Feb. 15 Reacquired 3,000 shares of $1 par common stock into treasury for $33,000 cash. Mar. 15 Reissued 2,000 shares of treasury stock for $24,000 cash. Aug. 15 Reissued 600 shares of treasury stock for $4,600 cash. Sept. 15 Declared (but did not yet pay) a $1 cash dividend on each outstanding share of common stock. Oct. 1 Issued 100, 10-year, $1,000 bonds, at a quoted bond price of 101. Oct. 3 Wrote off a $500 balance due from a customer who went bankrupt.

Prepare the journal entries to record each transaction. Review the accounts as shown in the General Ledger and Trial Balance tabs. If no entry is required for a transaction/event, select "No journal entry required" in the first account field.

1

Issued 5,000 shares of $1 par common stock for $50,000 cash. Record the transaction.

2

Reacquired 3,000 shares of $1 par common stock into treasury for $33,000 cash. Record the transaction.

3

Reissued 2,000 shares of treasury stock for $24,000 cash. Record the transaction.

4

Reissued 600 shares of treasury stock for $4,600 cash. Record the transaction.

5

Declared (but did not yet pay) a $1 cash dividend on each outstanding share of common stock. Record the transaction.

6

Issued 100, 10-year, $1,000 bonds, at a quoted bond price of 101. Record the transaction.

7

Wrote off a $500 balance due from a customer who went bankrupt. Record the transaction.

8

Prepare the closing entry for Dividends. Record the transaction.

Each journal entry is posted automatically to the general ledger. Use the drop-down button to view the unadjusted, adjusted, or post-closing balances.

UnadjustedPost-closing Unadjusted

Unadjusted

Post-closing

Dates:Jan 01

Jan 01

Jan 31

Jan 01

Jan 31

Jan 15

Jan 31

Feb 15

Feb 28

Mar 15

Mar 31

Aug 15

Aug 31

Sep 15

Sep 30

Oct 01

Oct 03

Oct 31

to:Oct 03

Jan 01

Jan 31

Jan 01

Jan 31

Jan 15

Jan 31

Feb 15

Feb 28

Mar 15

Mar 31

Aug 15

Aug 31

Sep 15

Sep 30

Oct 01

Oct 03

Oct 31

| General Ledger Account | ||||||||||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

|

| |||||||||||||||||||||||||||||||

|

| |||||||||||||||||||||||||||||||

|

| |||||||||||||||||||||||||||||||

|

| |||||||||||||||||||||||||||||||

| ||||||||||||||||||||||||||||||||