Accounting ACCT 2610 Chapter Notes - Chapter 10-11: Interest Expense, Initial Public Offering, Preferred Stock

22 Feb 2017

School

Department

Course

Professor

Document Summary

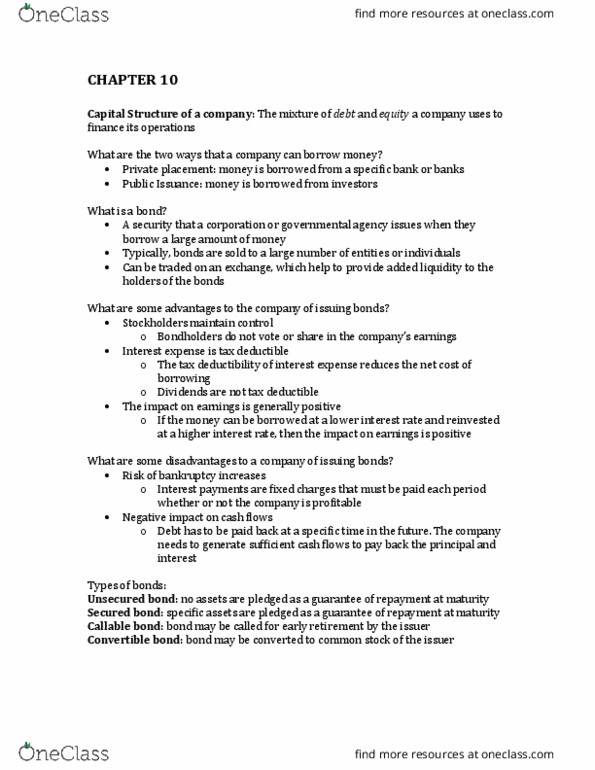

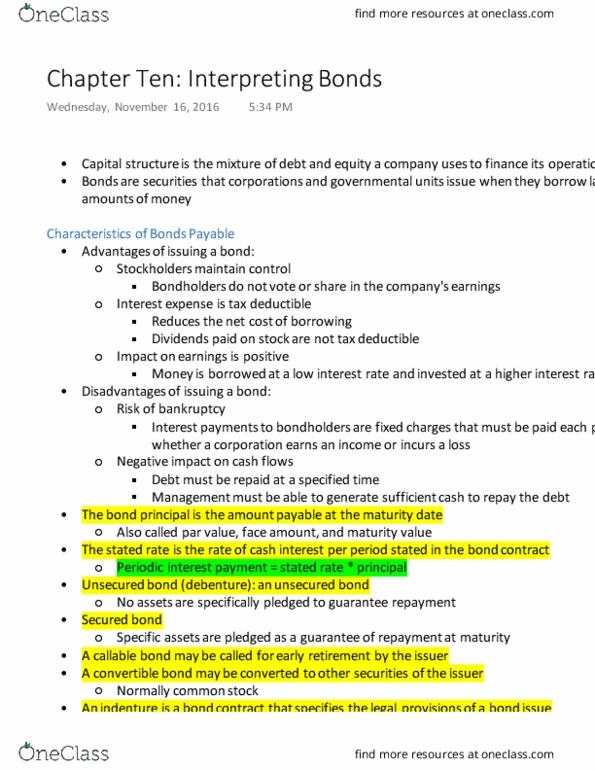

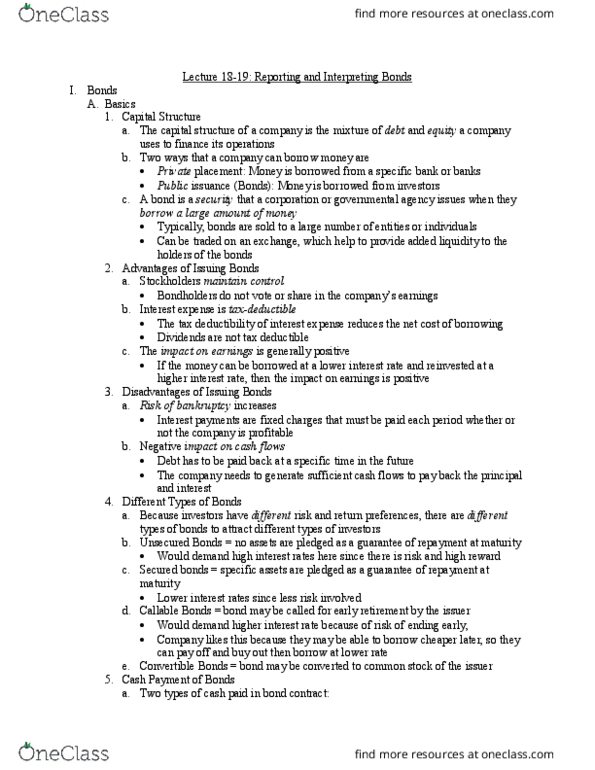

If stated rate=market rate, then face value=selling price. Single sum amount * pv factor= pv of single sum. Annuity amount * pv factor= pv of ordinary annuity. If stated rate > market rate, then bond is issued at premium: bond payable +premium on bond payable= book value. If stated rate < market rate, then bond is issued at a discount: bond payable- discount on bond payable= book value. Compute interest expense= nbv * market rate* n/12. Net book value= beginning book value + amortization expense: straight line. = (net income+interest expense +income tax expense)/interest expense: debt-to-equity. Authorized shares- max number of shares a corp. can legally sell to investors. Issued shares- total # of shares a corp. has sold to investors. Outstanding shares- total # of shares currently held by investors: common stock: basic voting stock issued by the corp. , owners of corp. Bene ts: a voice in management; dividends; residual claim.