MGAB01H3 Lecture Notes - Lecture 2: Ontario Securities Commission, Historical Cost, Financial Statement

MGAB01H3 verified notes

2/13View all

Document Summary

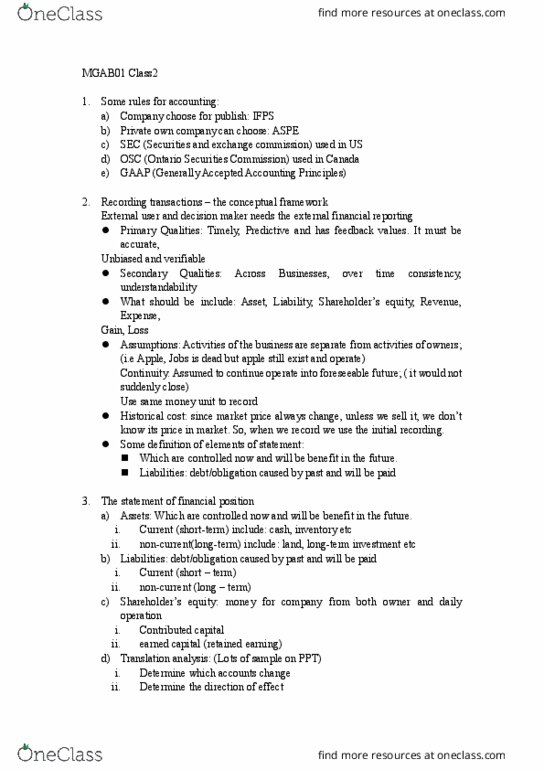

External user and decision maker needs the external financial reporting. Primary qualities: timely, predictive and has feedback values. Secondary qualities: across businesses, over time consistency, What should be include: asset, liability, shareholder"s equity, revenue, accurate, understandability. Assumptions: activities of the business are separate from activities of owners; (i. e apple, jobs is dead but apple still exist and operate) Continuity: assumed to continue operate into foreseeable future; ( it would not suddenly close) Historical cost: since market price always change, unless we sell it, we don"t know its price in market. So, when we record we use the initial recording. Which are controlled now and will be benefit in the future. Liabilities: debt/obligation caused by past and will be paid: the statement of financial position, assets: which are controlled now and will be benefit in the future. Current (short-term) include: cash, inventory etc non-current(long-term) include: land, long-term investment etc: liabilities: debt/obligation caused by past and will be paid.