EC223 Lecture Notes - Lecture 11: Economic Forecasting, Investment Advisory, Nominal Interest Rate

Document Summary

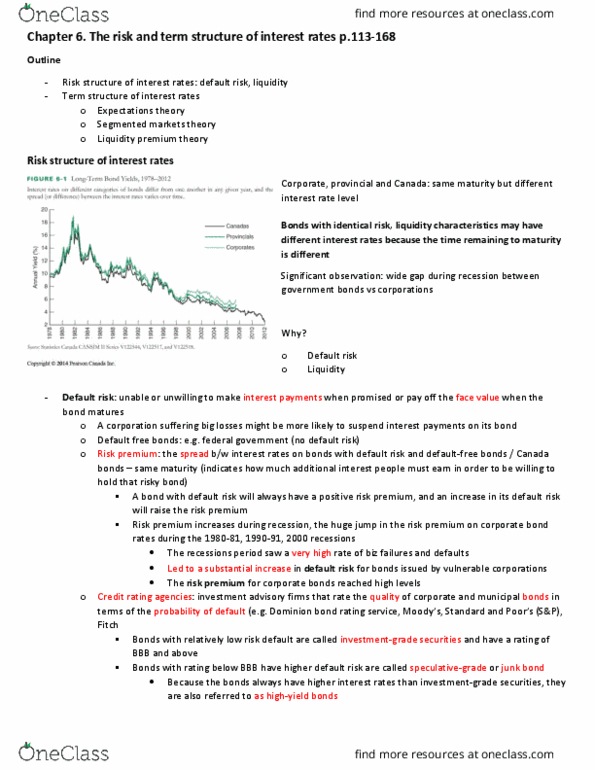

Week 6- chapter 6: the risk and term structure of interest rates. Long-term (cid:9)governm ent (cid:9)bond(cid:9)yields:(cid:9)10-year:(cid:9)main(cid:9)(including(cid:9)benchm ark)(cid:9)for t he(cid:9)unit ed(cid:9)st at es . Moody"s(cid:9)seasoned(cid:9)aaa(cid:9)corporat e(cid:9)bond(cid:9)yield t n e c r e. Indicates how much additional interest people must earn in order to be willing to hold that risky bond: the higher the default risk is, the higher the risk premium will be, credit rating agencies. Investment advisory firms that rate the quality of corporate and municipal in terms of the probability of default. Premiums during a recession: the huge spike in risk premiums on corporate bond rates between. 2002: the recession periods saw a very high rate of business failures and defaults. 8%/2) = 7: therefore, the interest rate on a 2-year bond must be at least 7% in order for you to be willing to purchase it, derivation, for an investment of .