ECON 1 Lecture Notes - Lecture 6: Average Variable Cost, Marginal Cost, Competitive Equilibrium

59 views2 pages

Verified Note

ECON 1 verified notes

6/31View all

Document Summary

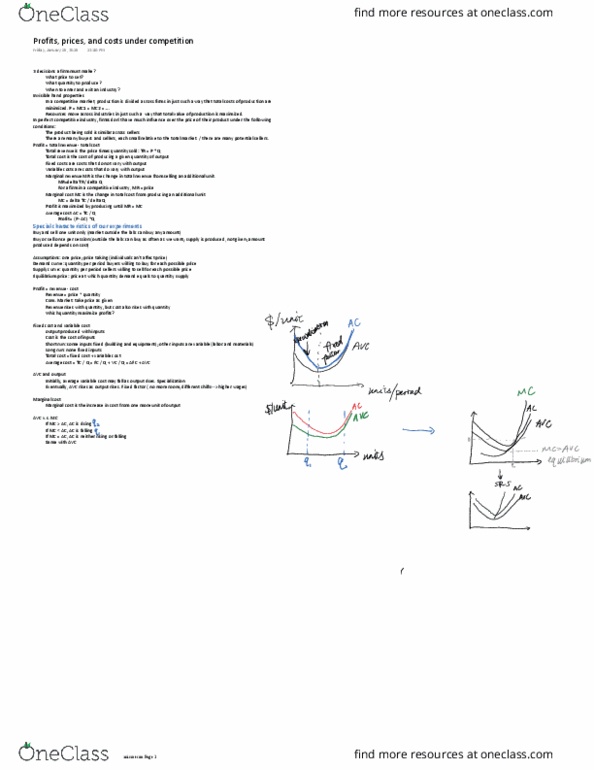

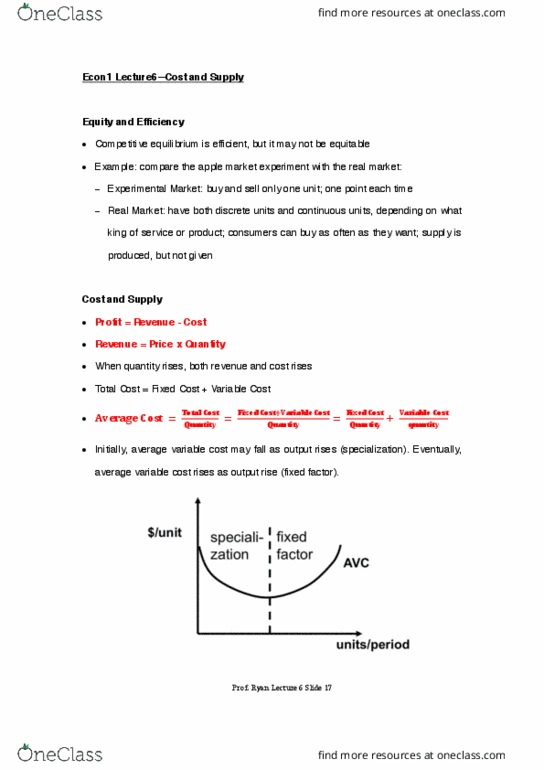

Equity and efficiency: competitive equilibrium is efficient, but it may not be equitable, example: compare the apple market experiment with the real market: Experimental market: buy and sell only one unit; one point each time. Real market: have both discrete units and continuous units, depending on what king of service or product; consumers can buy as often as they want; supply is produced, but not given. Cost and supply: profit = revenue - cost, revenue = price x quantity, when quantity rises, both revenue and cost rises, total cost = fixed cost + variable cost. Initially, average variable cost may fall as output rises (specialization). Eventually, average variable cost rises as output rise (fixed factor). Marginal cost: definition: the increase in cost from one more unit of output. If marginal cost > average cost, average cost is rising. If marginal cost < average cost, average cost is falling.

Get access

Grade+

$40 USD/m

Billed monthly

Homework Help

Study Guides

Textbook Solutions

Class Notes

Textbook Notes

Booster Class

10 Verified Answers

Class+

$30 USD/m

Billed monthly

Homework Help

Study Guides

Textbook Solutions

Class Notes

Textbook Notes

Booster Class

7 Verified Answers