ACCT 211 Chapter 6: Chapter 6 Fact Sheet

19 Jul 2016

School

Department

Course

Professor

Document Summary

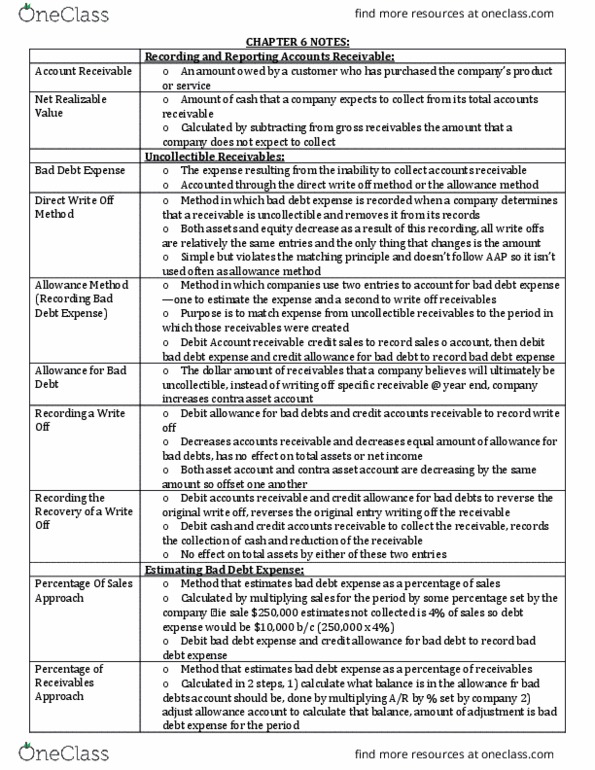

Accounts receivable: a company"s claim on the assets of another entity. Not all receivables are collected = bad debts. Bad debt expense is considered an operating expense and is usually combined with other expenses on the income statement. Net realizable value: is the amount of cash that a company expects to collect from its total or gross accounts receivable balance. Uncollectible account: a specific amount of receivables that is written off (the company has recognized that they will not receive the cash from the customer) Two methods: direct write-off method & the allowance method: timing: the method used will determine when to recognize the bad debt expense (1) establish account receivable: Accounts receivable . 3012130121$ (3) customer pays with a sales discount: Sales 3012130121$ (2) company determines that it will be unable to collect the money: What"s wrong with this method? (1) fails to match expenses with revenue (2) allows companies to manipulate earnings by period.