ACCT 211 Chapter Notes - Chapter 7: Perpetual Inventory, Accounts Payable, Current Asset

30 Aug 2016

School

Department

Course

Professor

Document Summary

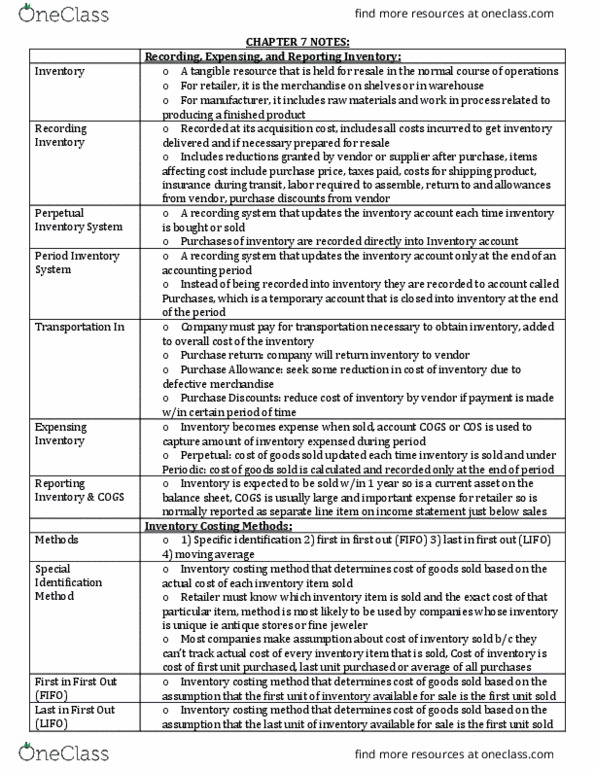

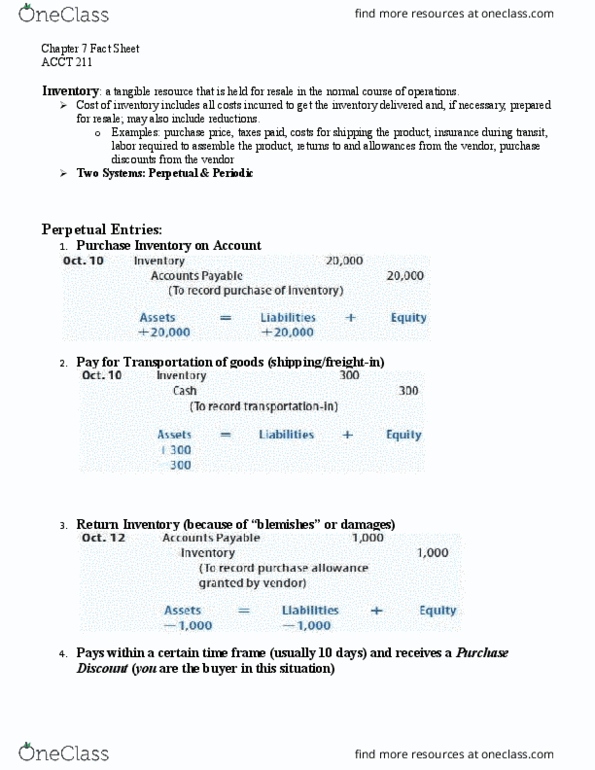

Inventory is a tangible resource that is held for resale in the normal course of operations. For a retailer, inventory is the merchandise on the shelves or in the warehouse. For the manufacturer, inventory also includes the raw materials and work in process related to producing a finished product. The phrase intended for sale differentiates inventory from other operational assets. Following the cost principle, inventory is recorded at its acquisition. Includes all costs incurred to get the delivery delivered and, if necessary, prepared for resale. Also includes any restrictions granted by the vendor or supplier after purchase. When inventory is purchased, a company will use either a perpetual inventory system or a periodic inventory system to record the inventory into its accounting system. A perpetual inventory system updates the inventory account each time inventory is bought or sold. Purchases of inventory are recorded directly into the inventory account.