ACCT 211 Chapter 7: Chapter 7 Fact Sheet (2)

19 Jul 2016

School

Department

Course

Professor

Document Summary

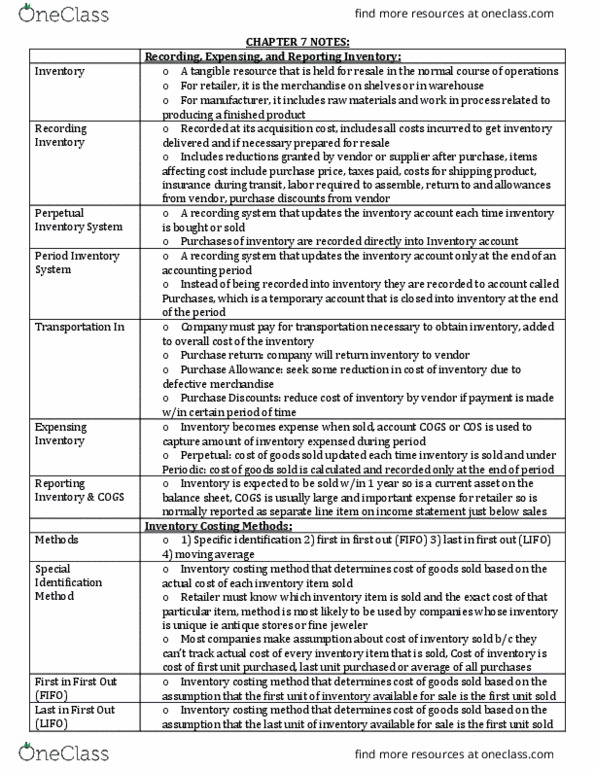

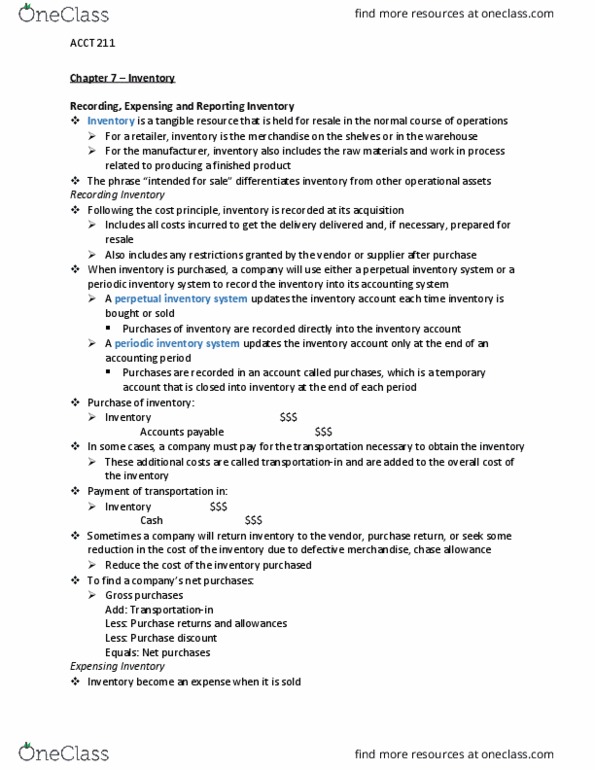

Inventory: a tangible resource that is held for resale in the normal course of operations. Perpetual entries: purchase inventory on account, pay for transportation of goods (shipping/freight-in, return inventory (because of blemishes or damages, pays within a certain time frame (usually 10 days) and receives a purchase. Both transportation and purchase discounts/returns and allowances are recorded as part of inventory in the general journal. So when calculating net purchases, you"re adding shipping, subtracting purchase returns & allowances/discounts to get the final net purchase balance, since the company considers these accounts as part of inventory. One for recording the sale of goods (revenue) One for recording the cost of goods (expense) Example: suppose snowy owl sells inventory costing for cash. Snowy owl would record the sale with the following two entries. When the company records the cost of goods sold on september 10th (when they sell. 65 units), they assume the first units sell first.