ACCT I S 211 Chapter Notes - Chapter 10: Chief Operating Officer, Cash Flow Statement, Cash Flow

13 Oct 2016

School

Department

Course

Professor

Document Summary

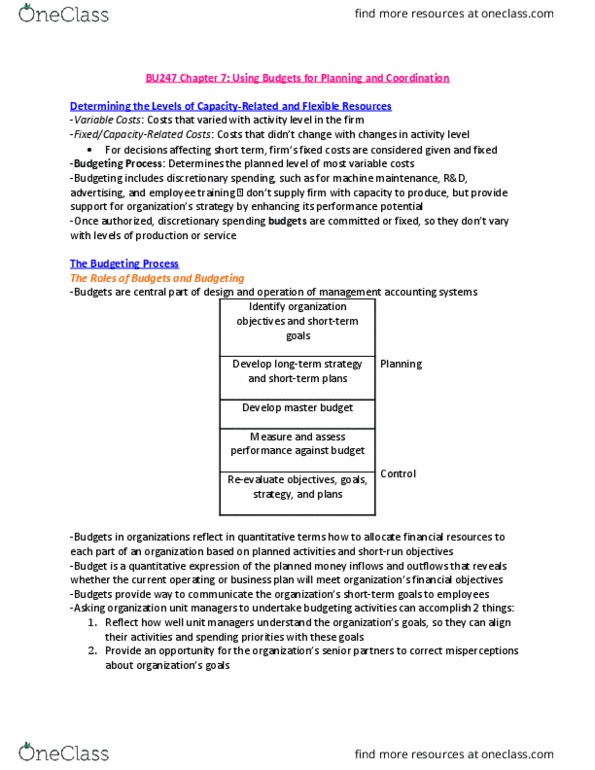

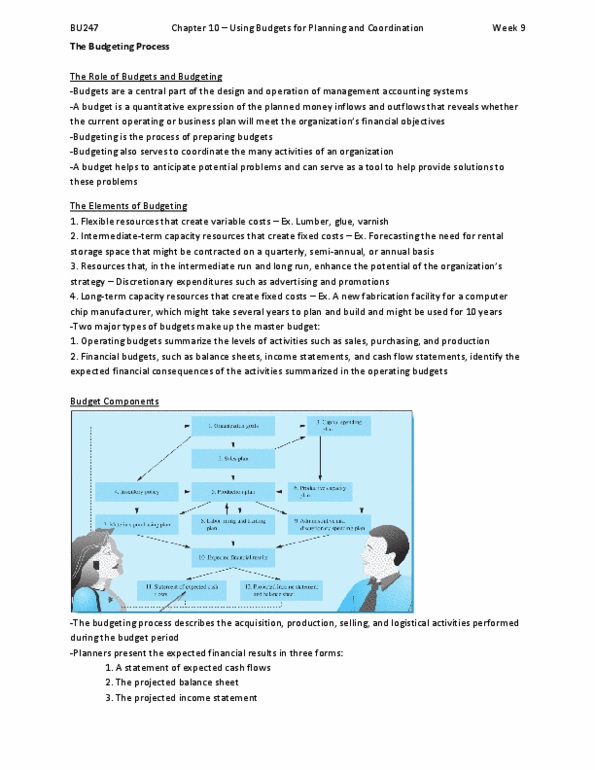

Determining the levels of capacity-related and flexible resources. Budgeting process- determines the planned level of most variable costs. Once authorized, discretionary spending budgets become fixed meaning they do not vary with levels of production or service. The role of budgets and budgeting: a budget is a quantitative expression of the planned money inflows and outflows that reveals whether the current operating or business plan will meet the organization"s financial objectives. Planning tool: communication device, coordinate activities, anticipate problems and develop crossfunctional solutions. What are the steps associated with setting up a budget: setting up a budgets is split into five parts in 2 categories: Why would you ask your managers to aid in budgeting activities: asking organization unit managers to undertake budgeting activities can accomplish 2 things: Reflect how well unit managers understand the organization"s goals, so that they can align their activities and spending priorities with those goals.