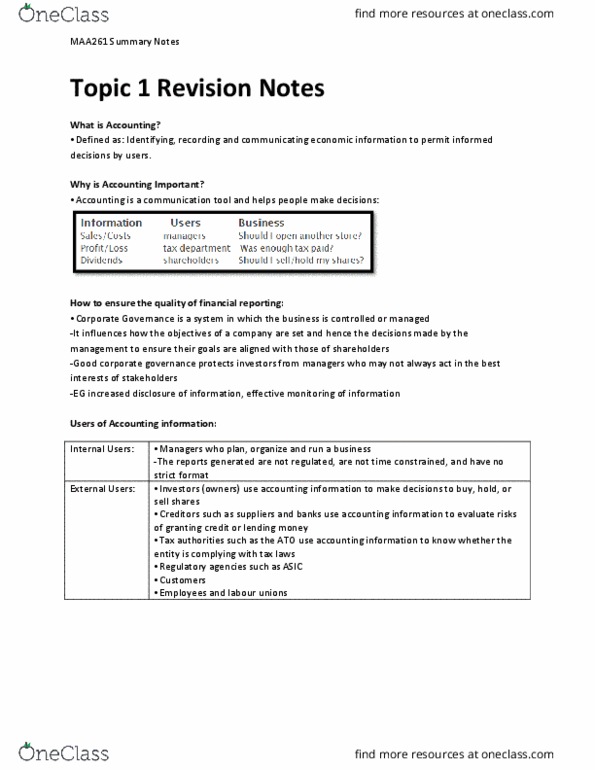

MAA261 Lecture Notes - Lecture 1: International Financial Reporting Standards, Financial Statement, Conceptual Framework

Document Summary

Identify the bodies involved in the development of accounting regulation in australia resulting in the issue of accounting standards. Financial reporting council (frc) oversees accounting standards board. Australian accounting standards board (aasb: corporations law. International accounting standards board (iasb: role and responsibilities. Australian securities and investment commission (asic: maintain, facilitate and improve the performance of the financial system and entities in it, administer and enforce the law, make info about companies publicly available. Explain the nature of the conceptual framework for financial reporting. Initially australia had its own conceptual framework consisting of 4 statements of accounting concepts (called sac 1-4: when australia adopted international financial reporting standards (ifrs) it also adopted. Ia b(cid:859)s (cid:862)fra(cid:373)e(cid:449)ork for the preparatio(cid:374) a(cid:374)d prese(cid:374)tatio(cid:374) of fi(cid:374)a(cid:374)(cid:272)ial state(cid:373)e(cid:374)ts(cid:863) Ia b(cid:859)s fra(cid:373)e(cid:449)ork replaced sac 3 and 4 but sac 1 and 2 were retained: more recently sac2 has been replaced. Define a reporting entity under the conceptual framework.