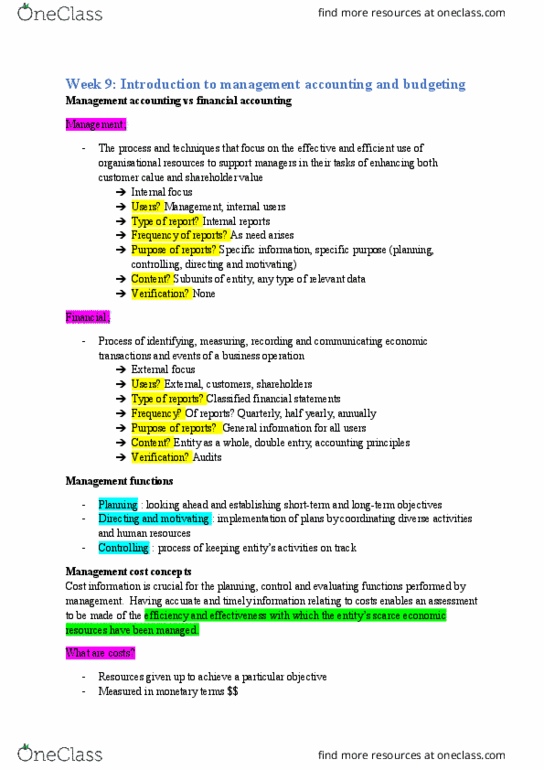

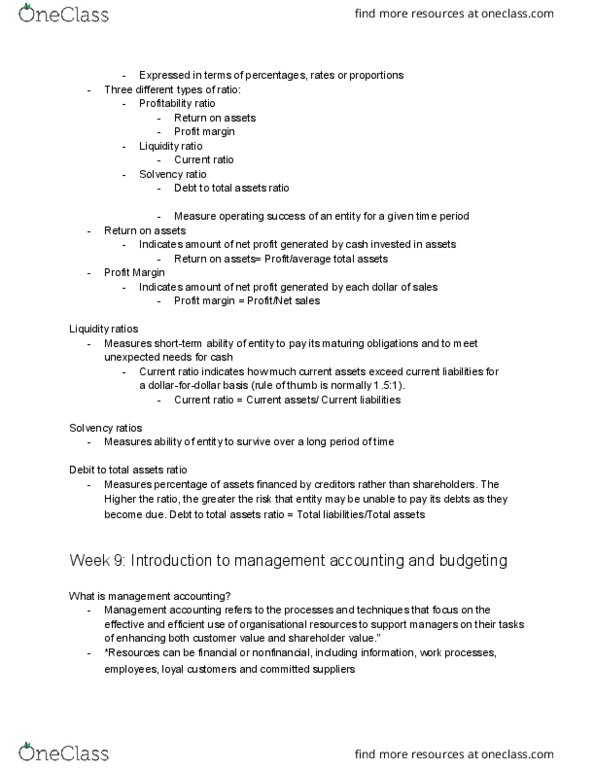

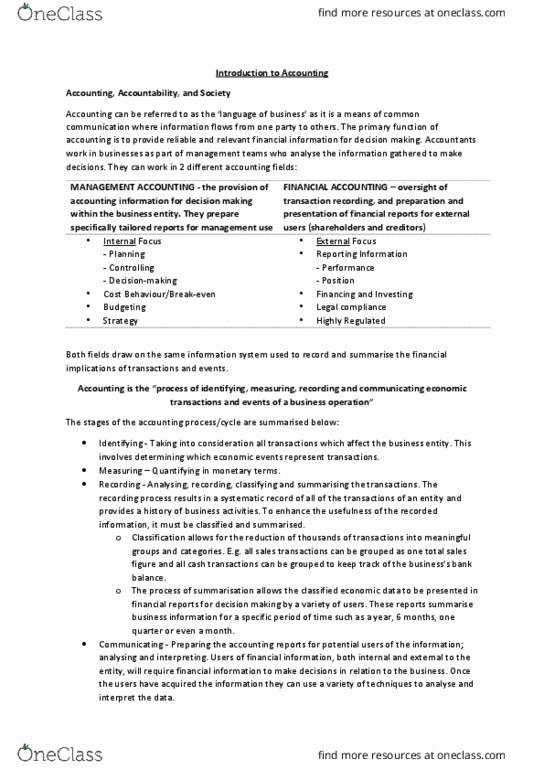

ACCG100 Lecture Notes - Lecture 9: High Standard Manufacturing Company, Management Accounting, Finished Good

11 May 2018

School

Department

Course

Professor

Management Accounting

An important similarity between management accounting and financial accounting is that each field

of accounting deals with the economic events of an entity. Moreover, both types of accounting

euie that the esults of a etit’s eooi eets e uatified ad ouiated to

interested parties.

However, diverse needs for economic data among users have let to the differences between the two

fields. Additionally, entities are often unwilling to disclose publicly sensitive information which may

be useful to competitors. Therefore, management accounting / managerial accounting refers to the

processes and techniques that focus on the effective and efficient use of organisational resources to

support managers in their tasks of enhancing both customer value and shareholder value. It applies

to all types of business (service, merchandising, manufacturing etc.) and all forms of business.

Traditionally, management accountants provided information that enabled management to make

decisions. Today, because globalisation and changes in technology, management accountants act

more as the strategic financial management professionals who integrate accounting expertise with

advanced management skills to drive business performance inside entities. They serve as trusted

partners to executives in all areas, offing the expertise and analysis necessary for sound business

decisions, planning, and support.

Management accountants need to adhere to a high standard of ethical conduct. Australia does not

have a professional body specifically for management accountants, but many belong to the two

main accounting bodies: CA, and CPA. APESB also sets the code of ethics and professional standards

by which members must abide.

The management of an entity performs 3 broad functions:

1. Planning: Looking ahead and establishing short-term and long-term objectives. A key

objective is to add value to the business under its control, where value is measured by the

tadig pie of a opa’s shaes and the potential selling price of the company itself.

Other objectives could involve short term profit goals, market share, ethical commitments.

Planning also involves long term strategic objectives.

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

An important similarity between management accounting and financial accounting is that each field of accounting deals with the economic events of an entity. Moreover, both types of accounting (cid:396)e(cid:395)ui(cid:396)e that the (cid:396)esults of a(cid:374) e(cid:374)tit(cid:455)"s e(cid:272)o(cid:374)o(cid:373)i(cid:272) e(cid:448)e(cid:374)ts (cid:271)e (cid:395)ua(cid:374)tified a(cid:374)d (cid:272)o(cid:373)(cid:373)u(cid:374)i(cid:272)ated to interested parties. However, diverse needs for economic data among users have let to the differences between the two fields. Additionally, entities are often unwilling to disclose publicly sensitive information which may be useful to competitors. Therefore, management accounting / managerial accounting refers to the processes and techniques that focus on the effective and efficient use of organisational resources to support managers in their tasks of enhancing both customer value and shareholder value. It applies to all types of business (service, merchandising, manufacturing etc. ) and all forms of business. Traditionally, management accountants provided information that enabled management to make decisions.