BSB110 Lecture Notes - Lecture 4: General Ledger, Accounting Equation, Trial Balance

Accounting – The Recording Process

Steps in the recording process

- Analyse each transaction in terms of its effect on the accounts

- Enter the transaction information in a journal

- Transfer the journal information (post) to the appropriate accounts in the ledger

Transactions and Events

- Occurrences which must be recorded because they have an effect on the assets, liabilities,

or equity items of a business

- Transactions – external exchanges of something of value between two or more entities

- Events – price increases in assets during an accounting period or allocation of cost of long-

lived assets of entities to different accounting periods

- Effect assets, liabilities, and equity

- Only record transactions which have a financial effect

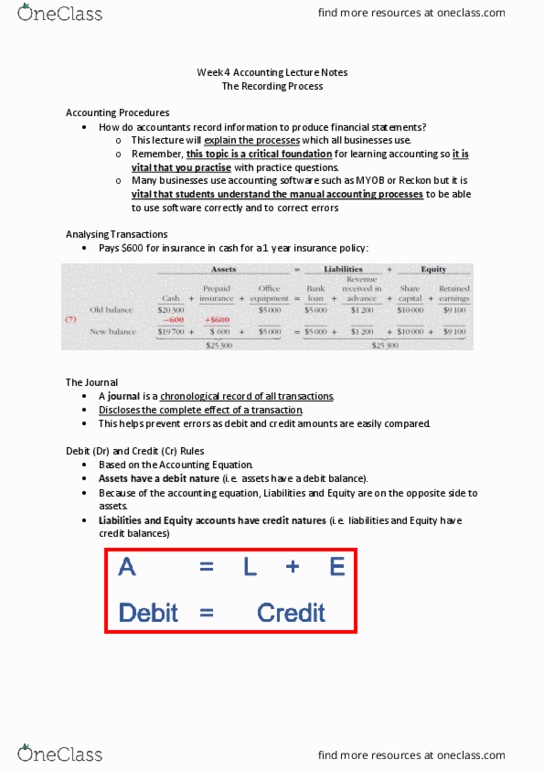

Analysing transactions

- Transaction analysis – the process of identifying the specific effects of transactions and

events on the accounting equation

- Is there an economic effect? E.g. purchasing Equipment – yes, hiring new employee – no

- What accounts are affected? – Assets, Liabilities, Equity

- The amount to be recorded

- Must always be a balance in Accounting Equation (Assets = Liabilities + Equity)

- The cause of each change in equity must be indicated

Journalising transactions

- Journal – chronological record of all transactions

- Discloses complete effect of transaction – prevents errors

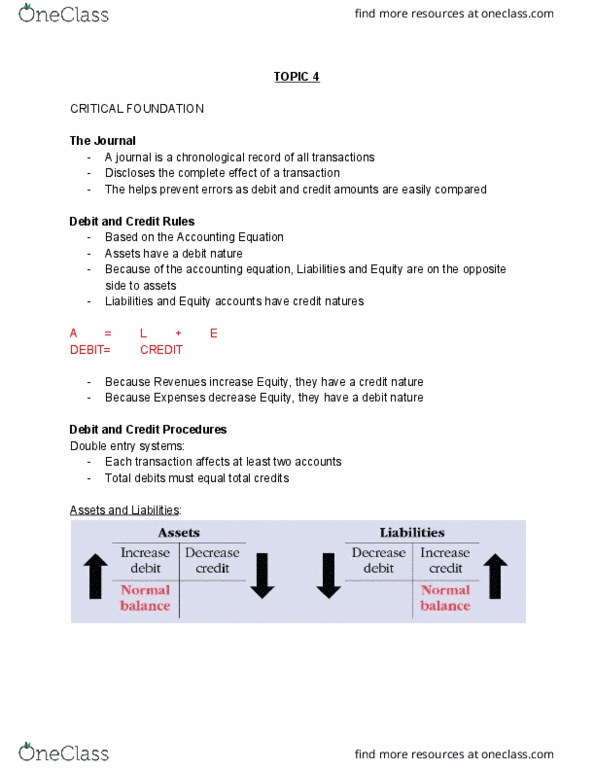

- Debit and Credit

oAccounting equation

oAssets and Expenses – Dr

oLiabilities, Equity, and Revenue – Cr

- Double Entry system

oEach transaction affects at least two accounts

oTotal debits must equal total credits

oWhen a debit account increases, a credit account must decrease

oWhen a credit account increases, a debit account must decrease

- Entering transactions

oThink about previous analysis – outline which accounts are affected and by how

much

oDoes the account need to be debited or credited?

- General ledger – contains all assets, liabilities, and equity accounts

- Chart of accounts – list of all accounts used in the general ledger

Posting Information to the ledger

- Ledger – contains all asset, liability, equity, revenue, and expense accounts

- Account

oIndividual accounting record of increases and decreases in a specific asset, liability or

equity item

oConsists of three parts

Name of the account

Left/debit side

Right/credit side

oAlso known as a T account

- Debit – posted to the left side

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

Analyse each transaction in terms of its effect on the accounts. Transfer the journal information (post) to the appropriate accounts in the ledger. Occurrences which must be recorded because they have an effect on the assets, liabilities, or equity items of a business. Transactions external exchanges of something of value between two or more entities. Events price increases in assets during an accounting period or allocation of cost of long- lived assets of entities to different accounting periods. Only record transactions which have a financial effect. Transaction analysis the process of identifying the specific effects of transactions and events on the accounting equation. E. g. purchasing equipment yes, hiring new employee no. Must always be a balance in accounting equation (assets = liabilities + equity) The cause of each change in equity must be indicated. Discloses complete effect of transaction prevents errors. Debit and credit: accounting equation, assets and expenses dr, liabilities, equity, and revenue cr.